⚡ TL;DR: When comparing Jewelers Mutual vs Hodinkee insurance, the best choice depends on your collection. Hodinkee (backed by Chubb) is best for modern collectors wanting instant, app-based coverage with zero appraisals required for watches under $100,000 and up to 150% market appreciation protection. Jewelers Mutual is best for traditional buyers who want an established, century-old standalone policy that covers repairs and replacements through a trusted local jeweler network.

• Compare how Jewelers Mutual and Hodinkee differ on coverage and claims

• Understand when cash payouts beat replacement sourcing

• Decide which insurer better protects high‑value watches

If you are trying to decide between jewelers mutual vs hodinkee insurance, the right choice ultimately comes down to how you wear, store, and value your collection.Look, if you’re still relying on homeowners insurance to protect that Submariner or Nautilus, we need to talk. Most standard policies cap jewelry coverage between $1,000 and $5,000 total.

You paid $15,000 for your watch. Your insurer hands you $1,500 when it’s stolen.

That’s not protection — that’s exposure.

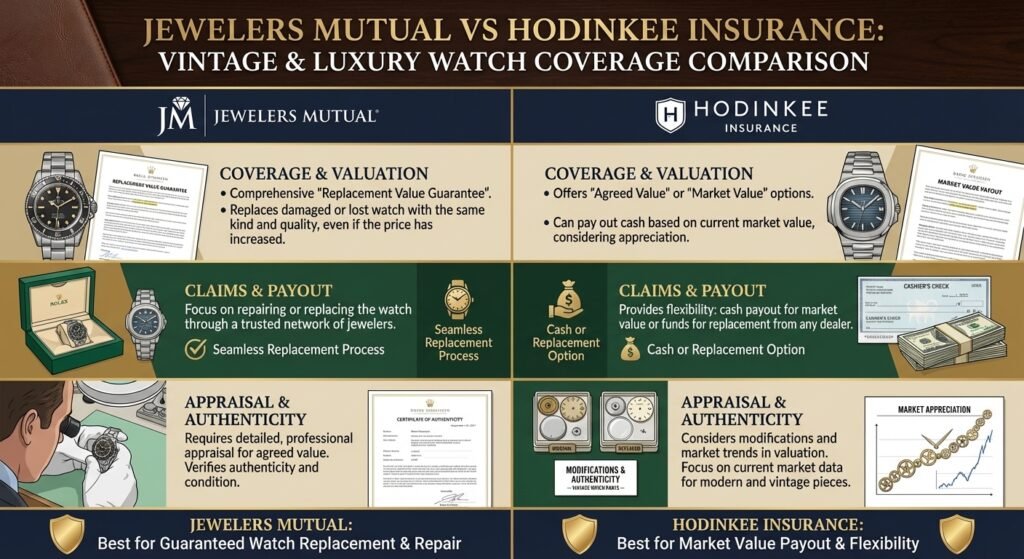

There are really only two names serious collectors debate when it comes to luxury watch insurance: Jewelers Mutual and Hodinkee Insurance (underwritten by Chubb). Both offer legitimate coverage, but they operate very differently — and that difference matters.

Question: Is Jewelers Mutual or Hodinkee better for watch insurance?

Answer:

It depends on your preference for claims handling. Hodinkee typically pays cash at agreed value, while Jewelers Mutual often sources a replacement watch, which can matter for discontinued or appreciating models.

🔍 Related Deep Dives

Before you choose between Hodinkee and Jewelers Mutual, read our other top-rated insurance guides:

Rolex Insurance Cost: What You Should Actually Be Paying

The Brutal Truth: WonderCare Luxury Insurance (2026)

Overview: How These Two Actually Work

Jewelers Mutual is the traditional specialist. They focus on replacing your lost or damaged watch with the same model.

Hodinkee Insurance takes the opposite approach. They pay you the agreed value in cash, and you decide what to buy next.

For collectors with appreciating or discontinued pieces, that flexibility can be critical.

Feature Comparison: What You’re Actually Getting

Both companies offer all‑risk coverage, including theft, accidental damage, and mysterious disappearance — something homeowners policies typically exclude.

Hodinkee includes appreciation protection up to 150% of insured value. If your watch appreciates significantly, you’re not stuck with outdated coverage.

Jewelers Mutual insures based on replacement sourcing. If the market moves and replacements cost more, gaps can appear.

CTA 1

Compare agreed‑value cash coverage against replacement‑based insurance to see which approach fits your collection.

Deductibles, Premiums, and Travel Coverage

Both companies offer zero‑deductible options. Hodinkee only offers zero deductible. Jewelers Mutual allows deductibles in exchange for slightly lower premiums.

Worldwide travel coverage is standard for both, which is essential for collectors who wear watches internationally.

Appraisal and Documentation Requirements

Hodinkee requires appraisals only for watches over $100,000 and gives a 90‑day grace period.

Jewelers Mutual often requires appraisals at lower thresholds, increasing setup friction for larger collections.

Claims Experience: Cash vs Replacement Reality

Claims handling is where philosophy becomes reality.

Hodinkee pays cash via ACH transfer. Jewelers Mutual attempts to source replacements.

For discontinued or rare watches, replacement sourcing can become difficult.

According to U.S. insurance regulators, high‑value personal items often require separate scheduled coverage beyond standard homeowners policies.

Luxury Watch Insurance Cost Calculator

Estimate what luxury watch insurance may cost based on your collection value and travel habits. Get an instant premium estimate to protect your valuable timepieces.

Pricing Comparison

Both insurers charge roughly 1–2% of insured value annually.

Pricing differences are minor compared to coverage philosophy and claims handling.

Who Each Insurer Is Best For

Choose Hodinkee if you:

- Own multiple watches that may appreciate

- Prefer cash payouts

- Travel frequently

- Want fast digital management

Choose Jewelers Mutual if you:

- Own one or two watches

- Prefer replacement sourcing

- Want a traditional insurer relationship

Get quotes from both Hodinkee and Jewelers Mutual to see how coverage structure impacts your protection.

Why Standard Insurance Still Fails Collectors

Homeowners insurance caps coverage, applies deductibles, excludes travel losses, and penalizes claims with higher premiums.

That’s why luxury watch insurance exists.

Final Verdict: Jewelers Mutual vs Hodinkee Insurance

For most collectors in 2026, Hodinkee’s cash‑based, appreciation‑aware coverage offers better flexibility for modern collections.

If you want deeper context, review best luxury watch insurance options or compare providers in our BriteCo vs WAX Insurance analysis.

At the end of the day, comparing jewelers mutual vs hodinkee insurance proves that both providers offer top-tier, standalone protection for serious watch collectors.

People Also Ask (FAQ)

Which is cheaper, Jewelers Mutual or Hodinkee?

Pricing for both providers typically ranges from 1% to 2% of the total value of your watch per year. For example, insuring a $10,000 Rolex will generally cost between $100 and $200 annually with either company. Your exact premium will depend on your zip code and local theft rates, so it is highly recommended to pull a free online quote from both.

Do I need an appraisal for coverage?

This is the biggest difference between the two. Hodinkee (backed by Chubb) does not require any appraisals or original receipts for watches valued under $100,000—you simply upload a clear photo and the model number via their app. Jewelers Mutual typically requires a recent detailed receipt or a professional appraisal to bind the policy.

Is homeowners insurance better than jewelers mutual vs hodinkee insurance?

No. Standard homeowners insurance usually caps jewelry payouts at $1,000 to $2,000 and does not cover “mysterious disappearance” (simply losing the watch). Furthermore, filing a claim on your home policy will cause your monthly premium to spike. Both Jewelers Mutual and Hodinkee offer standalone policies, meaning a watch claim will never affect your home insurance rates.

Next Read

- The Brutal Truth: WonderCare Luxury Insurance (2026)

- Rolex Insurance Cost: Is It Actually Worth It?

- Best Luxury Watch Insurance in 2026

- WAX Insurance and the Modern Watch Collector’s Insurance Dilemma

Choose coverage designed for how you actually collect, travel, and wear your watches — not how insurers categorize household goods.