Review for Jewellers Mutual Group

Jewelers Mutual Group delivers comprehensive protection for high-value timepieces, covering theft, loss, damage, and mysterious disappearance worldwide. You get zero deductible options and coverage that extends to normal wear and tear.

The policy protects your watches during international travel without territorial restrictions.

Claims specialists understand the watch market and work directly with you to replace stolen or lost pieces. Every watch gets valued at current market rates, not purchase price, and the company handles everything from Rolex to vintage Patek Philippe.

Your homeowners policy caps jewelry at $1,500. Your Submariner cost $12,000.

That gap represents real financial risk.

Most people learn this coverage shortfall after something happens. You file a claim for a stolen watch and learn your policy covers a fraction of the actual value.

By then, you’ve already lost thousands.

Standard insurance treats watches like any other personal property. The limits stay artificially low, the exclusions pile up, and the deductibles eat into whatever coverage exists.

If you travel internationally, many policies stop covering your watches the moment you cross borders.

This creates a genuine problem for anyone who owns watches worth protecting.

Jewelers Mutual built their entire business around jewelry and watch insurance. They’ve operated since 1913, working exclusively with high-value pieces.

You’re not adding a rider to a general policy or explaining to an adjuster why your Nautilus costs six figures.

The question becomes whether their approach actually solves the coverage problems collectors face.

Features Overview

Worldwide Protection Without Geographic Limits

Your watches stay covered everywhere. You can wear your Daytona in Dubai, your Royal Oak in Switzerland, or your vintage Speedmaster in Tokyo.

The coverage follows your watches globally without territorial restrictions.

Standard homeowners policies typically limit coverage to your residence or include restricted coverage while traveling. Some policies reduce coverage percentages when you take items abroad.

Others exclude international coverage entirely.

Jewelers Mutual eliminates these restrictions. Your $50,000 collection gets the same protection whether you’re home in New York or attending an auction in Geneva.

Mysterious Disappearance Coverage

You can’t find your watch. You don’t know if someone stole it, if you lost it, or if it disappeared some other way.

Most insurance companies won’t pay these claims. They need proof of theft or specific evidence of what happened. If you simply can’t locate the watch, standard policies deny coverage.

Jewelers Mutual covers mysterious disappearance as a standard policy feature. You file a claim explaining the watch disappeared. They process the claim without requiring you to prove exactly how or where you lost it.

This matters considerably for watches you wear regularly. You take off your watch at a restaurant, at the gym, during travel.

Sometimes pieces disappear without a clear explanation.

Zero Deductible Options

Most insurance forces you to pay a deductible before coverage begins. You might have a $1,000 or $2,500 deductible on jewelry claims.

For a $10,000 watch, you receive $8,500 after the deductible.

Jewelers Mutual offers policies with $0 deductibles. When you file a claim, you receive full coverage from the first dollar of loss.

This removes friction from the claims process and confirms you get finish value.

You can choose higher deductibles if you want lower premiums. But the zero deductible option exists for people who prefer comprehensive coverage without cost-sharing.

Normal Wear and Tear Included

Watches experience wear through regular use. Clasps loosen, crystals scratch, crowns wear down.

These aren’t dramatic failures, just normal deterioration from wearing the watch.

Standard insurance excludes this entirely. They cover sudden, accidental damage but not gradual wear.

If your bracelet clasp fails after years of use, you pay for repairs yourself.

Jewelers Mutual includes normal wear and tear coverage. When your watch needs service or repair from regular use, the policy covers it.

This benefit alone separates them from competitors for people who actually wear their watches instead of storing them.

Coverage for Natural Disasters

Flood and earthquake damage typically gets excluded from standard policies. You need separate flood insurance, and earthquake coverage comes with high deductibles and limited availability.

Your watches get covered for flood and earthquake damage under Jewelers Mutual policies. If natural disasters damage your collection, you file a claim like any other covered event.

Luxury Watch Insurance Calculator

Protect Your Timepiece Investment

Calculate the estimated insurance value and premium for your luxury watch. Get instant quotes for comprehensive coverage including theft, loss, damage, and mysterious disappearance. Our specialized insurance is designed specifically for fine timepieces.

✓ Accidental Damage

✓ Loss & Mysterious Disappearance

✓ Worldwide Coverage

✓ No Deductible Option Available

Luxury watches are significant investments that can appreciate over time. Specialized jewelry insurance provides comprehensive protection that standard homeowners insurance often lacks, including coverage for mysterious disappearance and no depreciation.

Performance Analysis

How Claims Actually Work

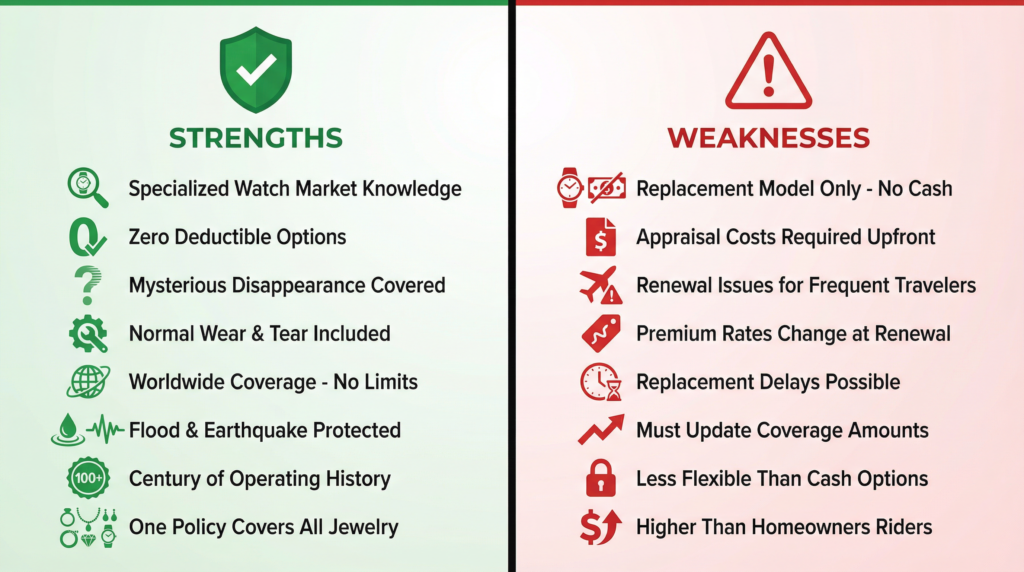

Jewelers Mutual focuses on replacement instead of cash payouts. When you file a claim, they work to find an identical or equivalent watch to replace your lost piece.

If they can’t find an exact replacement at the insured value, you face some decisions. You can add your own money to purchase the watch at current market price, or accept a different model valued at your policy limit.

One collector reported insuring a watch at $20,000 that later appreciated to $25,000. When the watch was stolen, Jewelers Mutual couldn’t source an identical replacement at the original insured value.

The collector needed to contribute additional funds to purchase at market price or select a different watch.

This differs from cash-based insurers like Hodinkee (underwritten by Chubb), which deposit the agreed value directly into your account. You receive money and handle sourcing the replacement yourself.

Some collectors prefer Jewelers Mutual’s approach because it guarantees you get an actual watch instead of managing the replacement process. Others find it restrictive compared to receiving cash and buying whatever you want.

Market Value Recognition

The company understands watches appreciate. They don’t treat your vintage Daytona like a generic timepiece or ignore market realities.

Claims adjusters know the difference between references, understand limited editions, and recognize how certain pieces gain value. This expertise matters when you file claims for watches that have increased significantly since purchase.

However, you need to update your coverage as values change. If you insured a watch at $15,000 five years ago and it’s now worth $30,000, your policy still pays based on the insured amount unless you’ve updated it.

Claims Processing Speed

Multiple policyholders report straightforward claims experiences. You send documentation online, email, or by phone.

The company responds within days typically, not weeks or months.

The timeline extends based on replacement availability. Finding an exact replacement for a discontinued Patek Philippe takes longer than replacing a current-production Rolex.

But the communication stays consistent throughout.

Compared to filing jewelry claims through standard homeowners insurance, collectors note the process moves faster and involves less back-and-forth documentation.

Travel Pattern Scrutiny

Some policyholders report Jewelers Mutual declined renewals after discovering frequent international travel. The company apparently assesses risk differently for internationally mobile collectors.

This creates potential uncertainty if your travel patterns change after purchasing the policy. You might get covered initially, then face renewal issues when they learn you travel extensively.

This concern appears in watch collector forums but isn’t universally reported. It stays unclear whether this reflects specific risk thresholds or isolated cases.

Pros and Cons

What Makes Jewelers Mutual Stand Out

Specialization creates real advantages. Claims adjusters understand horology, know current market values, and recognize why certain references command premiums. You don’t spend time educating insurance representatives about your collection.

Consolidated coverage simplifies management. You can insure watches, jewelry, engagement rings, and other valuables on one policy. High-net-worth people with diverse collections avoid juggling multiple specialized policies.

The company maintains financial stability. AM Best ratings and BBB credentials confirm they can pay claims years after issuing policies. This matters when you’re trusting a company to cover six-figure collections.

Customer service stays responsive. You can reach representatives through multiple channels, and the company maintains active social media presence for questions.

Where Jewelers Mutual Falls Short

The replacement model creates friction for investment-focused collectors. If you view watches primarily as appreciating assets, receiving a replacement watch instead of cash limits your options.

Appraisal requirements add cost and complexity. You need professional documentation for pieces over $5,000. These appraisals cost $40 to several hundred dollars depending on the watch.

For multiple pieces, this adds meaningful expense.

Travel-related renewal concerns need clarification. Before purchasing, you should discuss international travel patterns explicitly to avoid potential renewal issues.

You’re collaborating on replacements instead of receiving direct payment. Some collectors prefer handling their own sourcing as opposed to working with the insurance company to find replacement pieces.

User Experience

Getting Coverage Setup

The online quote process takes under 30 minutes typically. You enter information about your watches, their values, and your location.

The system generates premium estimates based on your zip code.

For watches over $5,000, you’ll need professional appraisals. You can’t simply upload receipts or claim a value.

This adds a step but confirms accurate coverage.

Once approved, your policy starts immediately. You receive documentation confirming coverage limits, deductibles (if any), and what’s included.

Managing Your Policy

You can add or remove watches as your collection changes. If you sell a piece or acquire something new, updating the policy takes minutes online or through a phone call.

Premium adjustments happen when you change coverage. Adding a $40,000 watch increases your annual premium by roughly $400-$800 depending on the rate.

The company sends renewal notices well in advance. You can adjust coverage limits at renewal to reflect appreciation or depreciation in your collection’s value.

Filing Claims When Something Happens

You report the loss online, by phone, or via email. You’ll need to provide documentation of the watch’s value (your appraisal), evidence of ownership (receipts, photos), and details about what happened.

For theft, police reports strengthen claims but aren’t always mandatory depending on circumstances. For mysterious disappearance, you explain when you last had the watch and when you uncovered it missing.

The company assigns an adjuster who contacts you within days typically. They explain next steps, what documentation they need, and timeline expectations.

For replacement-based claims, they begin sourcing an equivalent watch. They contact you with options when they find potential replacements.

For total loss situations where replacement isn’t possible, they process payment based on the insured value.

Value for Money

What You Actually Pay

Luxury watch insurance through Jewelers Mutual costs 1% to 2% of appraised value annually. A $10,000 Submariner runs $100 to $200 per year.

Your $75,000 Nautilus costs $750 to $1,500 annually.

These rates stay consistent across the industry. You’re not paying premium prices for the Jewelers Mutual brand specifically.

You’re buying their particular approach to claims and coverage features.

Geographic location affects rates. High-theft areas in major cities pay more than suburban or rural locations.

Your zip code decides the specific percentage within that 1-2% range.

Comparing Costs to Alternatives

Homeowners policy riders cost less, sometimes significantly. You might add $50,000 in jewelry coverage for $200-400 annually.

But filing claims affects your entire homeowners policy history and can increase rates across all your policies for years.

A $15,000 jewelry claim might raise your homeowners premium by $300-500 annually for the next three to five years. That $200 savings on the rider turns into $1,500-2,500 in increased homeowners costs over time.

Hodinkee insurance (underwritten by Chubb) typically costs slightly more than Jewelers Mutual but includes Investment Protection covering watches up to 150% of insured value. For appreciating collections, this added protection might justify higher premiums.

Going uninsured costs nothing until something happens. Then you absorb the full loss.

For a $50,000 collection, you’re risking substantial capital to save $500-1,000 annually.

Is the Premium Justified

You need to weigh the coverage features against annual cost. If you wear your watches regularly, travel internationally, and own pieces prone to appreciation, specialized coverage makes financial sense.

The mysterious disappearance coverage alone provides peace of mind worth the premium for many collectors. Knowing you’re covered regardless of circumstances removes anxiety about wearing valuable pieces.

For someone with one watch worth $8,000 who rarely travels and keeps it secure, a homeowners rider might suffice. For collectors with multiple pieces totaling $50,000+, dedicated coverage through Jewelers Mutual or similar specialists becomes necessary.

Final Verdict

Who Benefits Most From Jewelers Mutual

You own multiple watches valued between $5,000 and $100,000 each. You wear these watches regularly instead of keeping them stored. You travel domestically and internationally with your timepieces.

You also have other jewelry pieces worth insuring.

You want everything consolidated on one policy with zero administrative complexity.

Jewelers Mutual delivers exactly what you need. The worldwide coverage protects your watches wherever you go. The mysterious disappearance provision eliminates coverage gaps.

Normal wear and tear coverage helps maintain pieces you actually wear.

The zero deductible option removes friction from claims.

The replacement-focused approach works well if you’re not treating watches primarily as investment vehicles. You want an equivalent watch back, not cash to manage sourcing yourself.

When to Consider Alternatives

You view watches as appreciating investments and want most cash flexibility when filing claims. Your collection consists of rare, difficult-to-replace pieces where finding exact matches becomes problematic.

You prefer receiving direct payment and handling your own sourcing.

Hodinkee insurance (underwritten by Chubb) might serve you better. You receive cash payouts, get Investment Protection up to 150% for appreciation, and avoid the replacement negotiation process.

You own one watch worth under $25,000, don’t travel extensively, and want the absolute lowest premium cost. A homeowners policy rider provides basic coverage at reduced rates.

Just understand the claims will affect your homeowners insurance history.

The Bottom Line for Luxury Watch Insurance

Standard homeowners insurance leaves substantial gaps in coverage for valuable timepieces. You face coverage caps, mysterious disappearance exclusions, territorial restrictions, and deductibles that reduce claim values.

Jewelers Mutual addresses these gaps directly with policies designed specifically for high-value watches and jewelry. Their 110+ years of operating history, financial stability, and specialization in this niche create confidence they’ll honor claims when you need coverage.

The replacement approach instead of cash payouts represents the main trade-off. Some collectors appreciate this because it guarantees receiving an actual watch.

Others prefer the flexibility of cash-based choices.

For most collectors with substantial holdings, the annual premium justifies the protection. You remove anxiety about wearing valuable pieces, eliminate coverage gaps during travel, and protect against mysterious disappearance scenarios standard policies reject.

The right move involves comparing quotes directly. Get a Jewelers Mutual quote for your collection.

Compare that with Hodinkee’s offering.

Examine the premium difference and decide whether cash payout flexibility justifies any additional cost.

Most importantly, get proper coverage in place before something happens. The gap between your collection’s value and your homeowners policy limit represents real financial exposure you can eliminate for 1-2% of value annually.

Get your free Jewelers Mutual quote in under 30 minutes → Enter your collection details and receive instant premium estimates for comprehensive watch protection.

Compare Hodinkee insurance for cash-based claims → See if Chubb-underwritten coverage with Investment Protection better fits your collection.

Schedule a consultation with coverage specialists → Discuss your specific watches with advisors who understand luxury timepieces and can customize protection for your needs.

Your collection deserves protection that actually works. Standard coverage leaves you exposed. Specialized luxury watch insurance from Jewelers Mutual closes those gaps and let’s you wear your watches with confidence instead of constant worry about inadequate coverage.