⚡ TL;DR: Insuring a Rolex typically costs 1–2% of its value annually and protects against theft, loss, and accidental damage. For most owners who wear their watch regularly or travel often, the protection outweighs the premium — but self‑insurance may make sense if you rarely wear it and can easily absorb a total loss.

Introduction

Many Rolex owners hesitate when it comes to insurance.

Paying a few hundred dollars per year to protect something you already spent thousands on can feel unnecessary — until something happens.

Rolex watches are uniquely exposed assets:

• High resale value

• Globally recognizable

• Extremely portable

• Frequently targeted

The question isn’t emotional.

It’s financial.

The Core Financial Question

Is it worth insuring a Rolex?

For most owners, yes — especially if:

• The watch is worn weekly

• You travel with it

• Its value exceeds homeowners limits

• You cannot comfortably replace it

But let’s break this down with numbers.

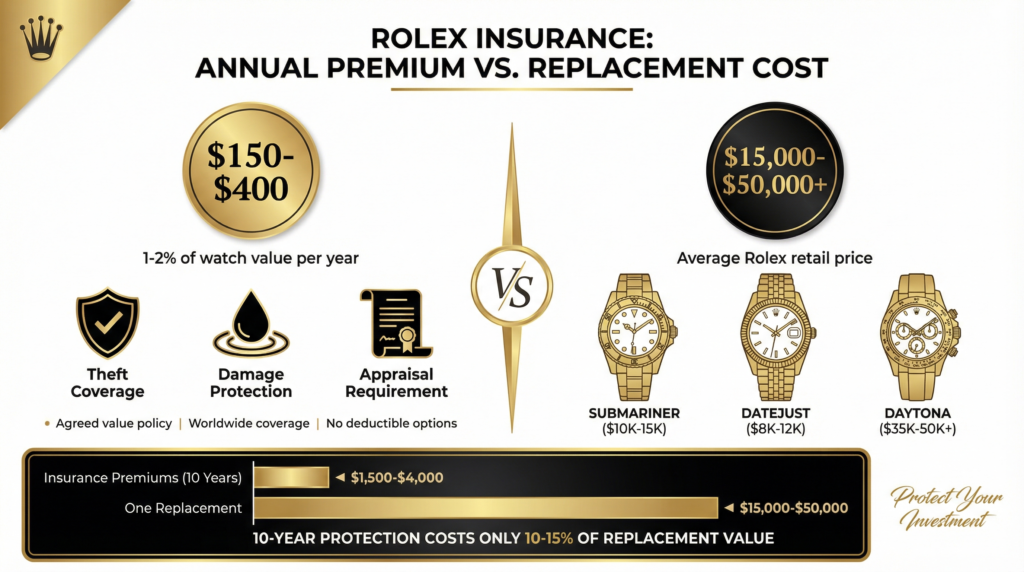

The Real Cost of Rolex Insurance

Specialty watch insurance typically costs:

1%–2% of the watch’s current market value per year

Example Cost Breakdown

| Rolex Value | Annual Premium | 5-Year Cost | 10-Year Cost |

|---|---|---|---|

| $8,000 | $80–$160 | $400–$800 | $800–$1,600 |

| $15,000 | $150–$300 | $750–$1,500 | $1,500–$3,000 |

| $25,000 | $250–$500 | $1,250–$2,500 | $2,500–$5,000 |

Now compare that to:

• One theft

• One loss

• One catastrophic accident

Why Rolex Watches Carry Elevated Risk

Rolex consistently ranks among the most stolen luxury watch brands.

Reasons:

• Recognizable branding

• Strong secondary market demand

• High value density

• Easy liquidity

Unlike a car or artwork, a Rolex can disappear in seconds.

Homeowners Insurance vs Specialty Coverage

Most homeowners policies:

• Cap jewelry coverage ($1,000–$5,000 typical)

• Apply deductibles

• Exclude mysterious disappearance

• Limit travel coverage

Specialty Rolex insurance typically includes:

• Agreed value payout

• Worldwide coverage

• Theft, loss, accidental damage

• Often no deductible

If your Rolex is worth $15,000 and your homeowners cap is $2,500, you are severely underinsured.

When Insurance Clearly Makes Sense

Insurance is strongly justified if:

✅ You wear your Rolex frequently

✅ You travel often

✅ The watch exceeds $5,000 in value

✅ You own high-demand models (Submariner, GMT, Daytona)

✅ You would feel financial strain replacing it

When It Might Not Be Worth It

Self‑insurance may make sense if:

• The watch stays in a safe deposit box

• You rarely wear it

• You can replace it without financial stress

• It falls under homeowners sublimits

But appreciation changes the equation.

Many Rolex models increase in value over time.

Decision Tool

Should You Insure Your Rolex?

Answer three quick questions to get a personalized recommendation on whether you should insure your luxury timepiece.

The Self‑Insurance Math

Example:

You insure a $15,000 Rolex

Premium = $200/year

After 10 years: $2,000 paid

Now ask:

Would losing $15,000 tomorrow hurt more than paying $200 per year?

That’s the real decision.

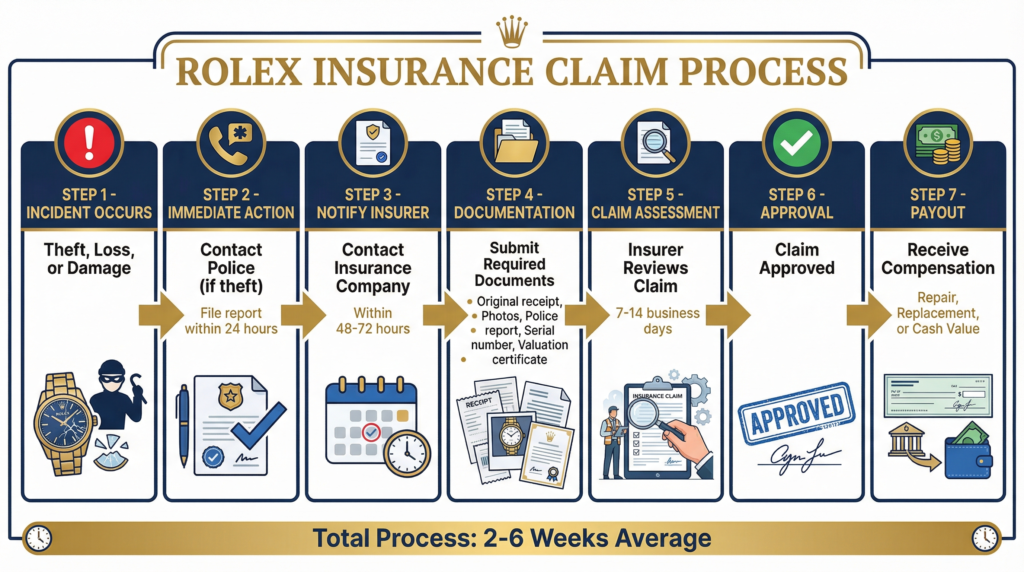

How Rolex Insurance Claims Typically Work

With specialty insurers:

• Value is agreed in advance

• Claims are faster than homeowners

• Documentation requirements are clear

• Adjusters understand luxury watches

This reduces post‑loss friction dramatically.

Final Verdict

For most Rolex owners, insurance is worth it.

The premium is predictable.

The risk is not.

If you actively wear your watch and travel with it, transferring that risk for 1–2% annually is financially rational.

Next Read

How Do I Insure My Rolex?

https://luxurywatchinsurance.net/how-to-insure-my-rolex/

Does Homeowners Insurance Cover Rolex Watches?

https://luxurywatchinsurance.net/does-homeowners-insurance-cover-rolex-watches/

How to File a Luxury Watch Insurance Claim

https://luxurywatchinsurance.net/how-to-file-a-luxury-watch-insurance-claim/