• Learn why professional appraisals are essential for proper watch insurance

• Understand how appraisers determine true replacement value

• Avoid costly underinsurance caused by outdated or incorrect valuations

I never thought about insuring my watches until I heard about my friend Marcus losing his grandfather’s Omega Seamaster during a business trip to London. The watch wasn’t especially valuable monetarily, but without a proper appraisal, even limited coverage was nearly impossible to claim.

That experience changed how I thought about protecting my own collection. Purchase receipts and assumptions about homeowners insurance simply aren’t enough when it comes to luxury watches.

Question: How do you appraise a watch for insurance?

Answer:

You appraise a watch for insurance by using a qualified watch appraiser who verifies authenticity, condition, and current market value. The appraisal establishes an agreed replacement value insurers use for coverage and claims.

Why Standard Insurance Fails Watch Collectors

Standard homeowners insurance policies are built for average household items, not high‑value timepieces.

Most policies cap jewelry and watch coverage at $1,000–$2,500 total and exclude mysterious disappearance and international travel losses. This is why luxury watch insurance exists.

Before any insurer will properly cover your watch, they need one critical document: a professional appraisal.

![[IMAGE 3 – INFOGRAPHIC]

ALT text: Infographic showing how watch appraisers evaluate authenticity, condition, and market value](https://luxurywatchinsurance.net/wp-content/uploads/2025/12/image_1766523154932_0-1-1024x559.jpeg)

Understanding What Appraisers Actually Evaluate

Professional appraisals go far

This documentation protects both you and the insurer during claims.

CTA 1

Compare insurance providers that require professional appraisals to ensure your watch is insured at true replacement value.

Finding an Appraiser Who Actually Knows Watches

Not all appraisers are qualified to assess luxury watches.

Look for appraisers with recognized credentials and specific watch expertise. Avoid appraisers affiliated with retailers or buyers, as conflicts of interest can lead to undervaluation.

Expect to pay $100–$300 per watch for a proper appraisal—an essential cost for serious collectors.

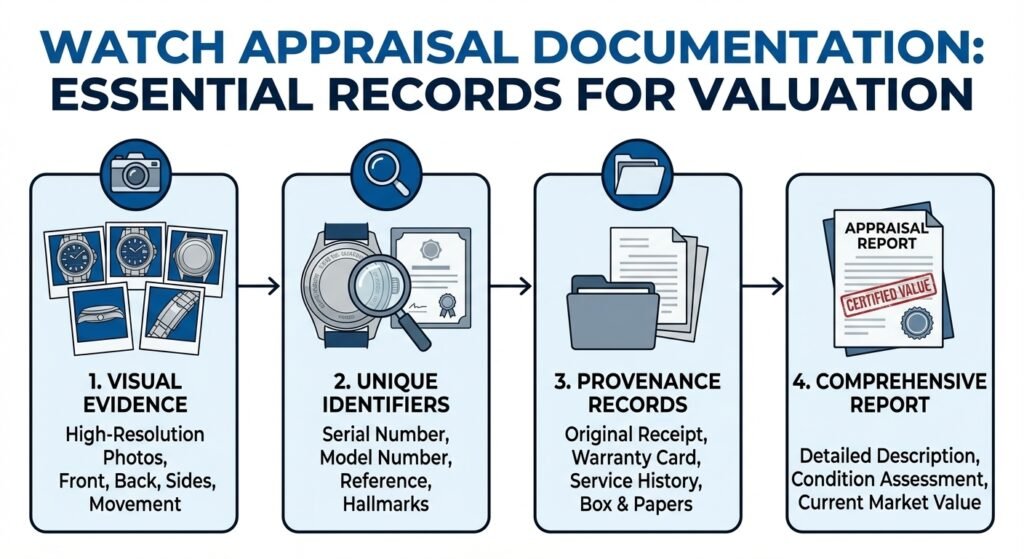

The Appraisal Process From Start to Finish

Bring everything to your appraisal: the watch, box, papers, service records, and receipts.

Appraisers photograph the watch extensively, inspect it with specialized tools, research comparable sales, and produce a detailed report establishing replacement value.

According to U.S. insurance regulators, high‑value personal items often require separate scheduled coverage beyond standard homeowners policies.

Luxury Watch Insurance Cost Calculator

Estimate what insuring your luxury or vintage watch may cost based on current market value.

CTA 2

Estimate what proper insurance coverage should cost and compare quotes before choosing a policy.

How Market Dynamics Affect Your Coverage

Watch values change rapidly. Appreciation can leave you dangerously underinsured if appraisals aren’t updated.

Update appraisals every two to three years—or sooner for rapidly appreciating models.

Documentation Beyond the Appraisal

Maintain detailed records: purchase documents, service history, photographs, and provenance. Store copies securely in multiple locations.

This documentation is critical for successful claims and ownership verification.

Different Types of Insurance Coverage

Scheduled endorsements on homeowners policies offer limited protection.

Specialized collector policies provide broader coverage including mysterious disappearance, international travel, and accidental damage.

Ultra‑high‑value collections may qualify for fine art and collectibles policies.

Frequently Asked Questions

Can I use a purchase receipt instead of an appraisal?

No. Receipts don’t establish current replacement value or authenticity.

How often should appraisals be updated?

Every two to three years, or sooner if values rise significantly.

Do modified watches affect insurance?

Yes. Modifications must be disclosed and documented accurately.

Key Takeaways

Professional appraisals form the foundation of proper luxury watch insurance.

Standard homeowners insurance is inadequate for valuable timepieces.

Regular revaluations, documentation, and agreed value coverage prevent catastrophic underinsurance.

CTA 3

Protect your watch collection by securing insurance built for luxury timepieces—not household goods.