• Learn why vintage and heirloom watches require a different insurance approach

• Understand how valuation, provenance, and claims differ from modern watches

• Avoid costly mistakes that leave irreplaceable timepieces underinsured

I’ve been collecting watches for years now, and one thing I learned the hard way is that your grandmother’s 1960s Omega doesn’t fit neatly into modern insurance categories. Most people spend hours researching which luxury watch insurance provider to use for their brand-new Rolex, but when it comes to vintage and heirloom timepieces, the conversation gets complicated fast.

Vintage watches present unique challenges that contemporary pieces simply don’t. The market values fluctuate wildly based on condition, provenance, and collector trends. Replacement becomes nearly impossible for discontinued models, and the emotional value of heirloom watches carries weight no insurance payout can replace.

That’s why luxury watch insurance exists for collectors who own more than easily replaceable modern pieces.

Understanding the Vintage Watch Insurance Coverage

Vintage watches operate in a fundamentally different category than modern timepieces.

Unlike modern watches with clear retail pricing, vintage values depend on originality, condition, provenance, and recent auction results. Two visually similar watches can differ in value by thousands of dollars.

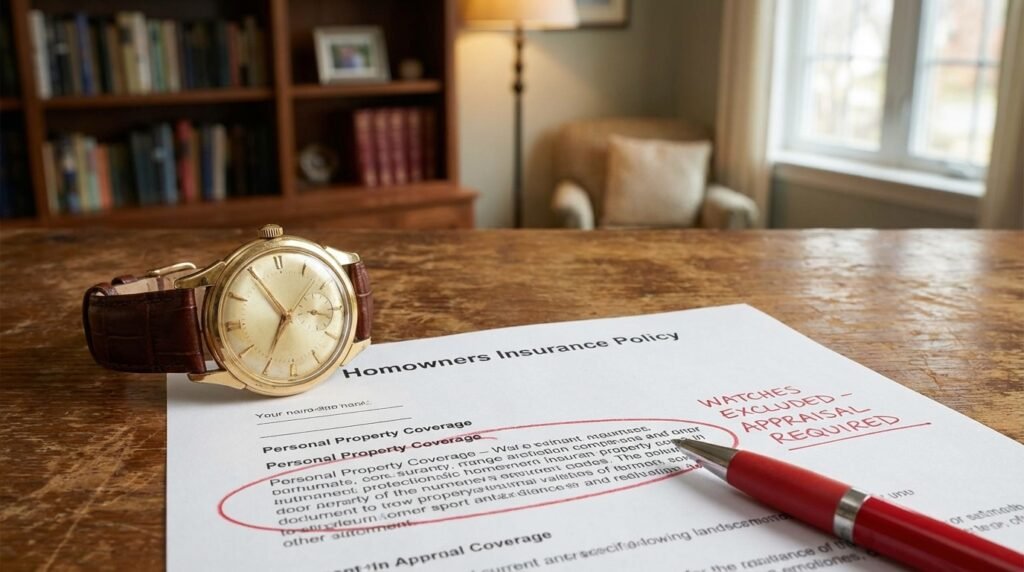

Standard homeowners policies cap watch coverage at $1,500–$5,000 total and rely on adjusters unfamiliar with horological nuance. Even scheduled riders struggle to address appreciation and replacement realities.

Collectors who insured vintage pieces for outdated values often discover painful gaps when claims occur.

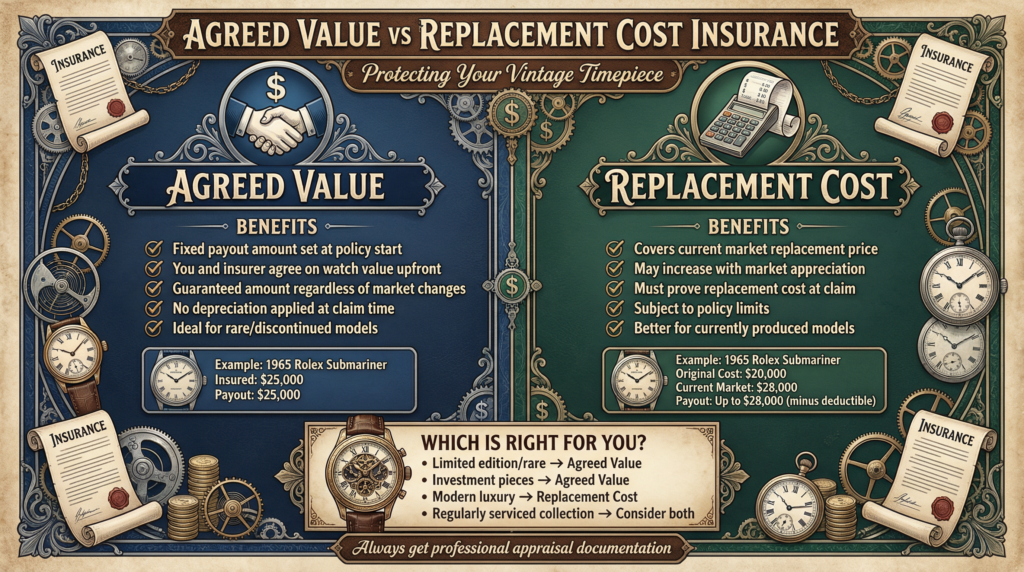

Agreed Value Policies vs Replacement Cost

This is the single most important insurance decision for vintage watches.

Agreed value policies lock in a payout amount upfront, eliminating disputes during claims. Replacement cost policies introduce ambiguity for irreplaceable timepieces and often result in undervalued settlements.

For vintage and heirloom watches, agreed value coverage is almost always the correct choice.

CTA 1

Compare insurers that offer true agreed value coverage for collectible and vintage watches.

Professional Appraisal Requirements

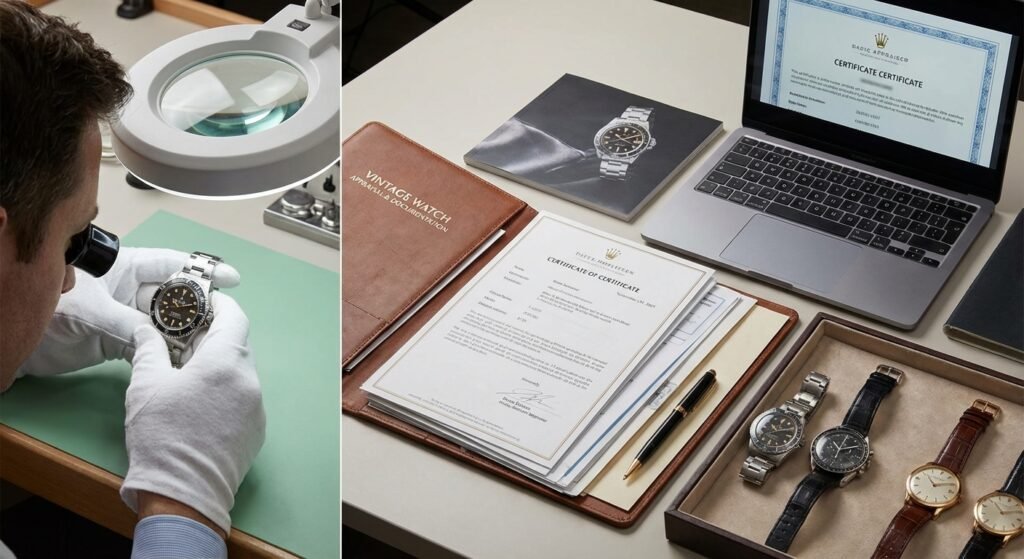

You cannot properly insure a vintage or heirloom watch without a professional appraisal.

Appraisals document originality, condition, serial numbers, component integrity, and recent comparable sales. This protects both valuation and claims outcomes.

Expect to update appraisals every three to five years, or more often for rapidly appreciating references.

Always confirm your insurer accepts the appraiser before commissioning work.

Documenting Provenance and History

Provenance can materially impact both value and claims outcomes.

Photograph every detail, store documentation securely, and preserve service records. Family history, original receipts, and correspondence strengthen insurance protection.

Keep duplicate records off-site or in cloud storage.

Handling Watches with Modified or Replaced Parts

Most vintage watches have experienced servicing or part replacement over decades.

Transparency is critical. Appraisers must document which components are original, period-correct replacements, or modern service parts.

Insuring a watch inaccurately creates major claim risk. Coverage must reflect true condition, not idealized assumptions.

How to Choose the Right Insurance Policy

Selecting the right policy means focusing on agreed value, worldwide coverage, mysterious disappearance protection, and claims expertise.

According to U.S. insurance regulators, high‑value personal items often require separate scheduled coverage beyond standard homeowners policies.

Luxury Watch Insurance Cost Calculator

Estimate what vintage or heirloom watch insurance may cost based on current market value and travel habits.

When comparing insurers, review best luxury watch insurance options and provider comparisons like BriteCo vs WAX Insurance to understand differences in valuation and claims handling.

CTA 2

Get quotes from specialty insurers experienced with vintage and heirloom watches before committing coverage.

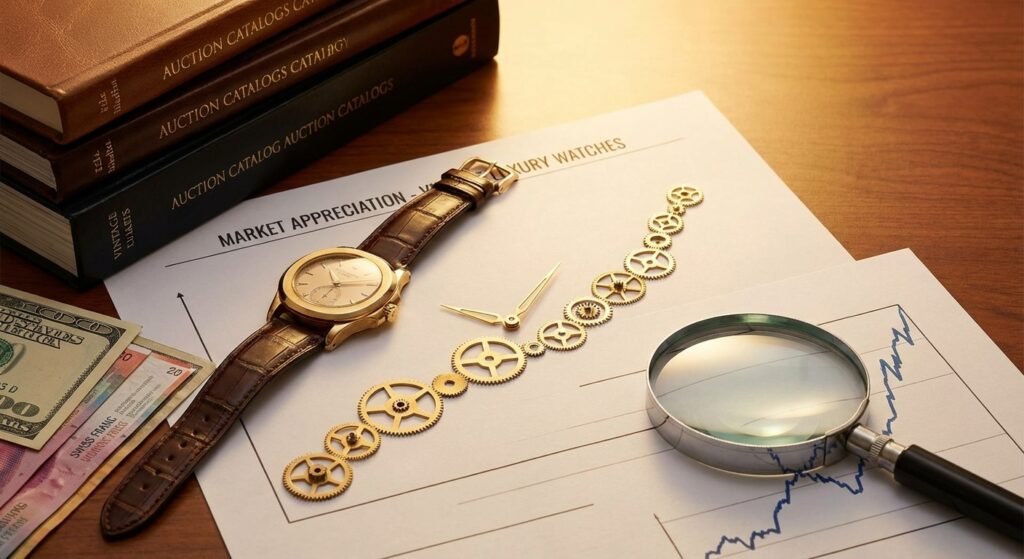

Common Concerns and Market Appreciation

Vintage watch values are volatile. Underinsurance is common when values double or triple between appraisals.

Some insurers offer appreciation buffers, but periodic revaluation remains essential.

Ignoring appreciation can expose collectors to six‑figure losses.

Key Takeaways

Vintage and heirloom watches require specialized insurance strategies focused on agreed value, documentation, and provenance.

Standard homeowners insurance is inadequate for collectible timepieces.

Professional appraisals, accurate disclosures, and regular policy reviews protect both financial and sentimental value.

CTA 3

Protect irreplaceable heirloom watches by choosing insurance built for collectibles—not household goods.