• Learn the most common insurance mistakes luxury watch owners make

• Understand how coverage gaps can cost you tens of thousands of dollars

• Protect your watch collection properly before a loss occurs

I’ve owned luxury watches for over a decade now, and figuring out the insurance situation was genuinely one of the most stressful parts of collecting. When I bought my first serious piece, a pre-owned Submariner, I assumed my regular home insurance had me covered.

That illusion shattered when a friend had his Daytona stolen and received barely a fraction of its value. That experience pushed me to dig deeply into luxury watch insurance—and what I discovered shocked me.

Question: What are the biggest watch insurance mistakes?

Answer:

The biggest watch insurance mistakes include relying on homeowners insurance, insuring for purchase price instead of current value, ignoring exclusions like mysterious disappearance, and failing to update coverage as values change.

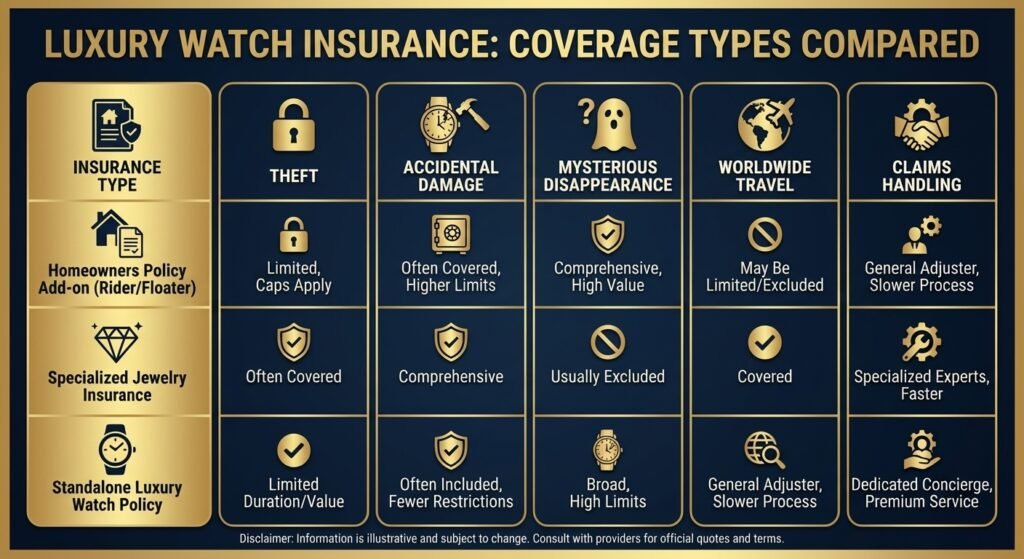

Understanding Why Standard Coverage Falls Short

Insurance companies treat luxury watches like everyday household items.

Standard homeowners policies cap jewelry coverage at $1,000–$5,000 total and often exclude mysterious disappearance and international travel. That’s why luxury watch insurance exists.

Mistake #1: Insuring for Purchase Price Instead of Market Value

Luxury watches often appreciate significantly.

If you insure a watch for what you paid instead of current market value, you’re exposed to massive shortfalls. Agreed value coverage is essential.

CTA 1

Compare insurance policies that use agreed value coverage to avoid being underinsured as watch values rise.

Mistake #2: Assuming Homeowners Insurance Covers Everything

Homeowners insurance often excludes mysterious disappearance and international travel.

A $15,000 watch may receive only a $2,500 payout after deductibles.

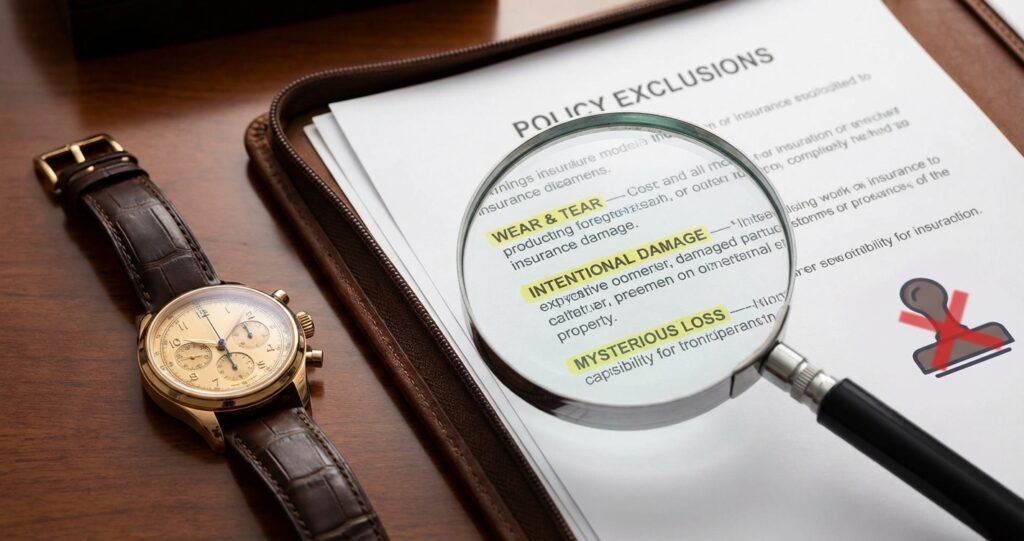

Mistake #3: Ignoring Policy Exclusions

Skipping the fine print leads to denied claims.

Wear and tear, mechanical failure from age, and security‑related exclusions are common.

Mistake #4: Never Updating Your Policy

Collections evolve. Market values change.

Annual policy reviews prevent underinsurance and wasted premiums.

Mistake #5: Confusing Warranty Coverage with Insurance

Warranties cover defects—not theft, loss, or accidental damage.

Insurance protects against real‑world risks.

Mistake #6: Ignoring Market Appreciation

Watch markets are volatile.

Some policies offer extended replacement coverage buffers, but regular reappraisals remain critical.

Mistake #7: Forgetting International Travel Coverage

Travel is when watches face the highest risk.

According to U.S. insurance regulators, high‑value personal items often require separate scheduled coverage beyond standard homeowners policies.

CTA 2

Get quotes from specialty insurers that include unlimited worldwide coverage and mysterious disappearance protection.

How to Choose the Right Insurance Policy

Look for:

- Agreed value coverage

- All‑risk protection

- Worldwide travel coverage

- Low or zero deductibles

Luxury Watch Insurance Cost Calculator

Estimate what luxury watch insurance may cost based on your collection and travel habits.

CTA 3

Estimate what proper luxury watch insurance should cost and compare providers before committing.

Key Takeaways

Luxury watch insurance costs about 1–2% of collection value annually and offers far better protection than homeowners policies.

Avoiding these mistakes can save you from devastating financial losses