• Why standard insurance rarely protects Rolex Submariner watches

• How Submariner values outgrow homeowners coverage

• What insurance features matter most for Submariner owners

⚡ TL;DR: Submariner owners need insurance that reflects rising market value and covers theft, water damage, and loss beyond homeowners limits.

Why Rolex Submariner Watches Require Specialized Insurance

Intro

The Rolex Submariner is one of the most recognized luxury watches in the world. Its durability, water resistance, and everyday wearability make it a favorite among collectors and first‑time Rolex buyers alike.

Those same characteristics also expose a major insurance problem. The Submariner is worn frequently, travels often, and holds substantial resale value. Standard homeowners insurance was never designed to protect an asset used this way.

Many Submariner owners assume they are insured simply because they have homeowners or renters coverage. In reality, this assumption creates one of the largest protection gaps in luxury watch ownership.

CTA #

Understanding how insurance treats the Rolex Submariner prevents costly surprises after theft or damage.

Overview

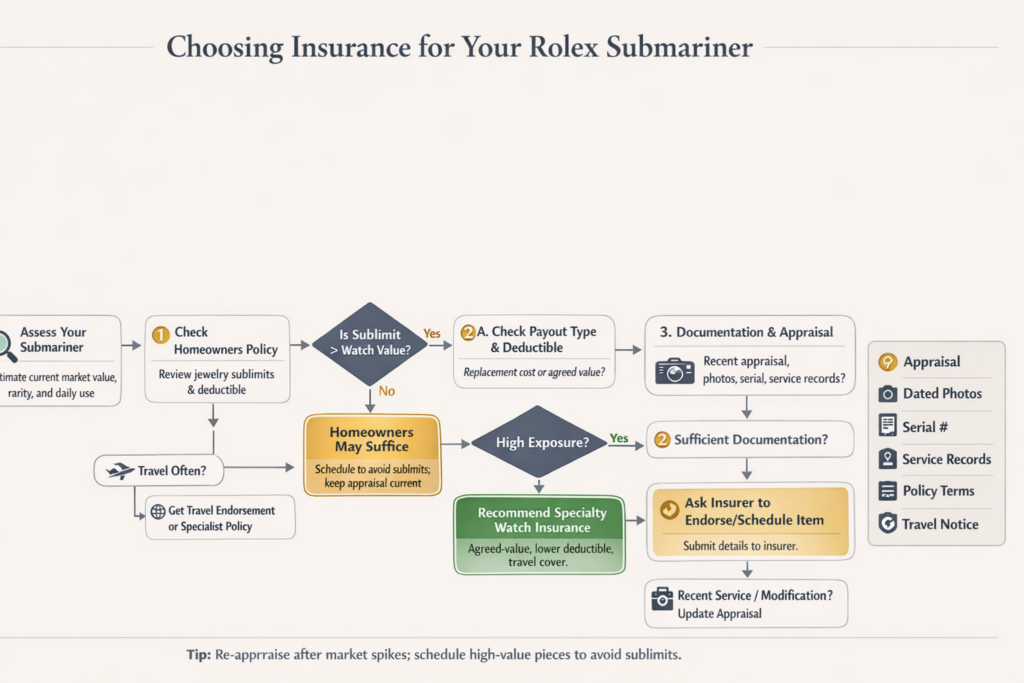

Homeowners insurance policies typically include limited coverage for jewelry and watches. These limits often fall far below the replacement value of a Rolex Submariner.

Specialty watch insurance is designed around high‑value timepieces that are worn, traveled with, and exposed to real‑world risks. Coverage structure, not brand reputation, determines outcomes.

A broader explanation of how luxury watch insurance works is available here:

https://luxurywatchinsurance.net/luxury-watch-insurance-coverage-2/

Question: Do Rolex Submariner watches need special insurance?

Answer: Yes. Rolex Submariner watches are often underinsured by homeowners policies due to low sublimits, exclusions, and rising market values.

At‑a‑Glance Quick Answers

• Submariners often exceed homeowners coverage limits

• Theft and damage are common risks

• Travel exposure increases loss probability

• Specialty insurance offers broader protection

• Documentation affects claim outcomes

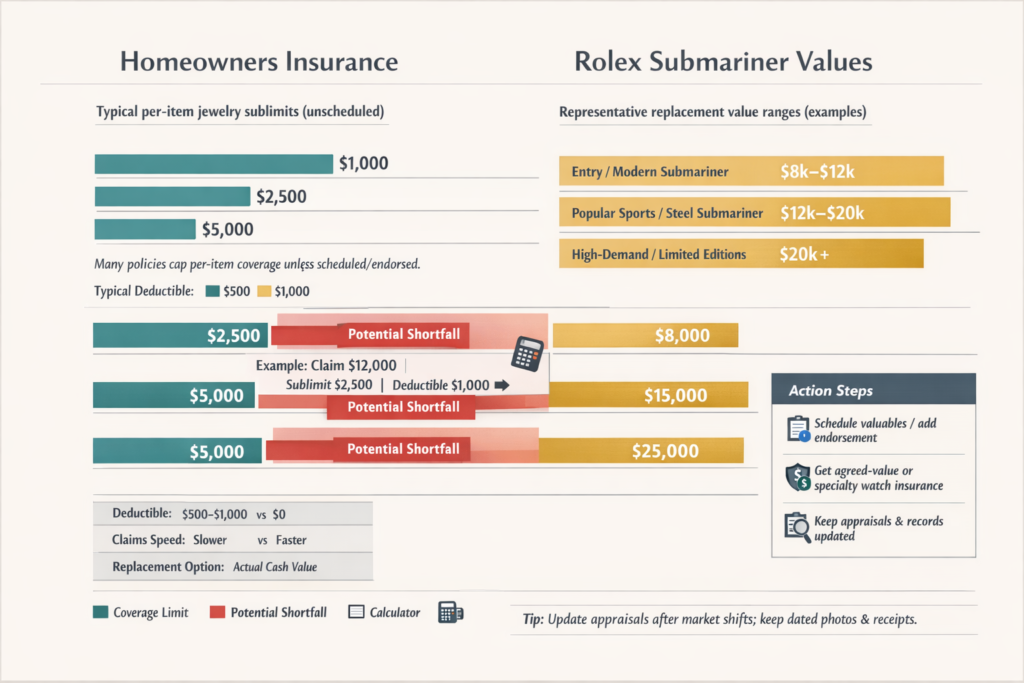

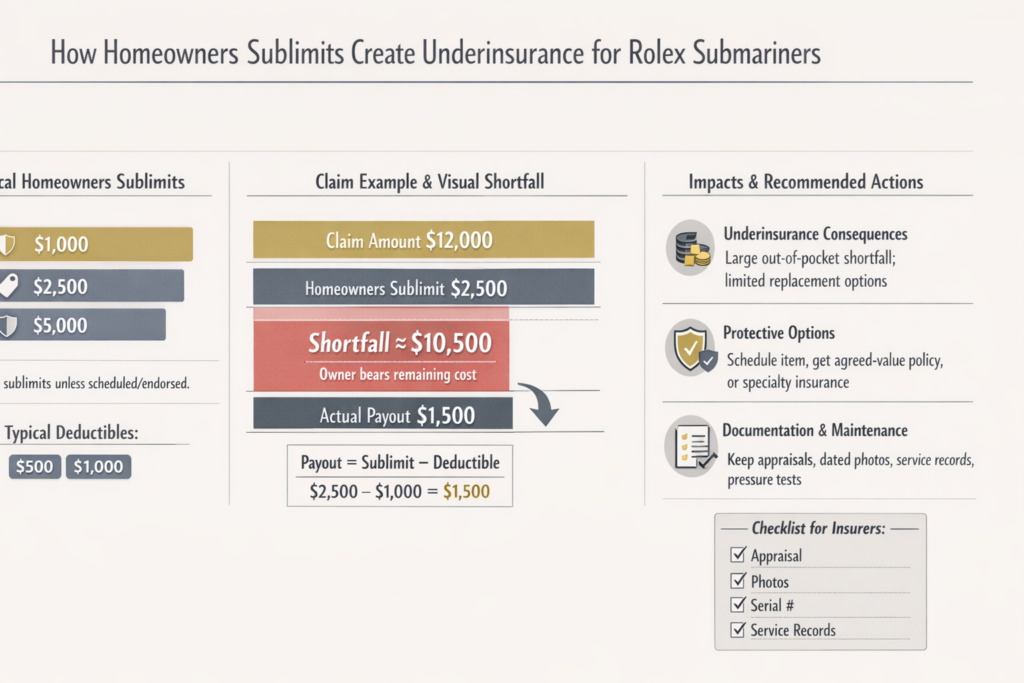

The Coverage Gap for Submariner Owners

Most homeowners policies cap jewelry coverage between $1,500 and $5,000 per item. These limits apply regardless of the watch’s actual value.

A Submariner purchased for $9,000 several years ago may now trade for $14,000 or more. Homeowners insurance still applies the same sublimit, creating an expanding coverage gap over time.

Scheduling the watch as a rider may increase limits, but often introduces deductibles, exclusions, and travel restrictions that still leave owners exposed.

CTA #

Coverage gaps grow automatically as Submariner values appreciate.

Submariner Risks Beyond the Home

Unlike dress watches, the Submariner is designed for activity. Owners swim, travel, and wear it daily. These environments increase exposure to theft, accidental damage, and loss.

Homeowners insurance often restricts coverage outside the residence or excludes international incidents. Many policies also exclude mysterious disappearance, one of the most common loss scenarios for frequently worn watches.

Specialty insurance typically provides worldwide coverage without geographic limitations.

Specialty insurers handling Submariner claims include:

https://luxurywatchinsurance.net/wondercare-luxury-insurance-review/

https://luxurywatchinsurance.net/hodinkee-watch-insurance-review-2/

CTA #

Insurance designed for travel reduces uncertainty when Submariners leave home.

All‑Risk Coverage Explained

Specialty watch insurance usually operates on an all‑risk basis. This means the policy covers loss or damage unless a specific exclusion applies.

For Submariner owners, covered scenarios often include:

• Theft at home and away

• Accidental damage from drops or impacts

• Water damage from sudden ingress

• Mysterious disappearance

• Fire and flood damage

This structure reflects real‑world Submariner use far better than named‑peril homeowners policies.

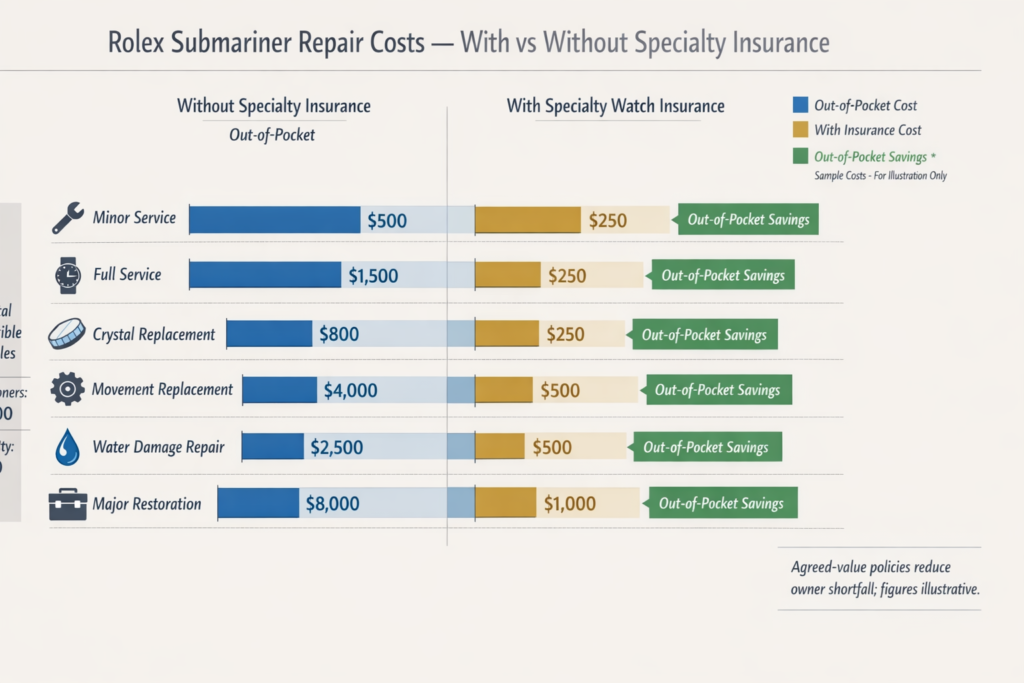

Repair Costs and Claims

Submariner repair costs can be significant.

• Crystal replacement: $500–$1,500

• Movement repairs: $2,000–$4,000

• Extensive corrosion or internal damage: $5,000+

Without insurance, these costs are paid out of pocket. Specialty insurers coordinate repairs through authorized service centers or approve cash settlements.

CTA #

Repair costs alone often exceed annual insurance premiums.

Documentation and Appraisals

Insurance coverage is only as strong as the documentation supporting it. Submariner owners should maintain:

• Serial numbers

• Purchase receipts

• Professional appraisals

• Clear photographs

• Service records

Documentation should be stored separately from the watch and backed up digitally.

For general consumer guidance on insurance claims and documentation standards, resources are available from the National Association of Insurance Commissioners:

https://www.naic.org/consumer_home.htm

Service History and Water Exposure

Water resistance relies on gasket integrity and crown sealing. Insurers may deny water damage claims if seals were not maintained over time.

Although Rolex recommends service approximately every ten years, frequent water exposure may justify more regular inspections. Service history often becomes evidence during claims.

Unauthorized service or aftermarket parts can complicate or void coverage entirely.

🔒 Rolex Submariner Insurance Fit Checker

Answer a few questions to see whether your current insurance is adequate for your Rolex Submariner. Get personalized recommendations to protect your investment.

📋 Recommended Next Steps

CTA #

Maintenance and documentation influence Submariner claim outcomes.

People Also Asked

Does homeowners insurance cover Rolex Submariner theft?

Usually only partially due to low jewelry sublimits.

How much does it cost to insure a Submariner?

Typically 1%–2% of current market value annually.

Is Submariner water damage covered?

Sudden accidental water damage may be covered; gradual damage is often excluded.

Can vintage Submariners be insured?

Yes, with professional appraisals reflecting originality and condition.

Does Rolex warranty cover loss or damage?

No. The warranty covers manufacturing defects only.

Key Takeaways

• Rolex Submariner watches are frequently underinsured

• Homeowners policies apply outdated limits

• Specialty insurance aligns with real‑world use

• Repair and replacement costs are significant

• Proper coverage protects both value and peace of mind

CTA #

Submariner owners benefit most when insurance decisions are made before a loss occurs.

Next Read

Luxury Watch Insurance Coverage Explained

https://luxurywatchinsurance.net/luxury-watch-insurance-coverage-2/

Best Luxury Watch Insurance in 2026

https://luxurywatchinsurance.net/best-luxury-watch-insurance-2026/