⚡ TL;DR: Luxury watch insurance typically covers theft at home at full value, while standard homeowners insurance often limits payouts through low jewelry sublimits and deductibles.

What You’ll Learn

• Learn whether home theft is covered under luxury watch insurance

• Understand why homeowners insurance often denies these claims

• Protect your watches against the most common at‑home loss scenarios

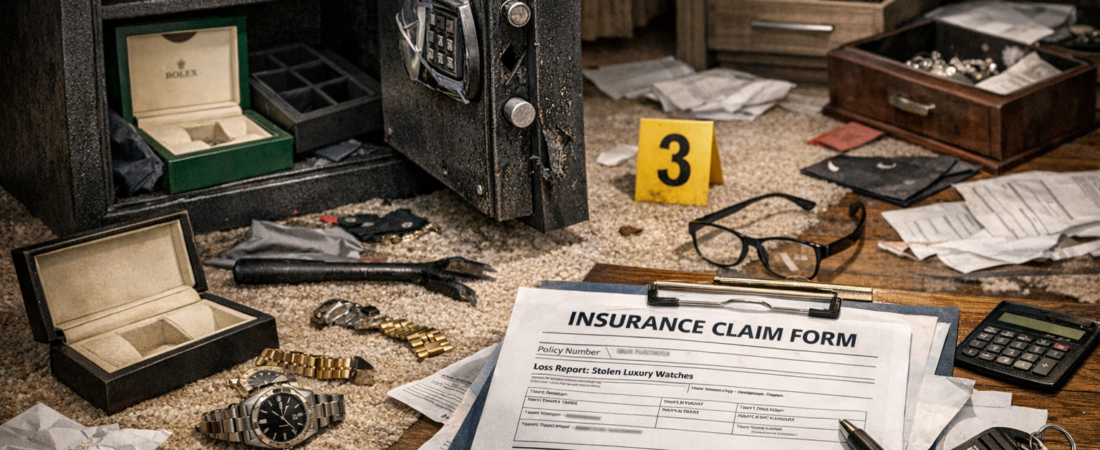

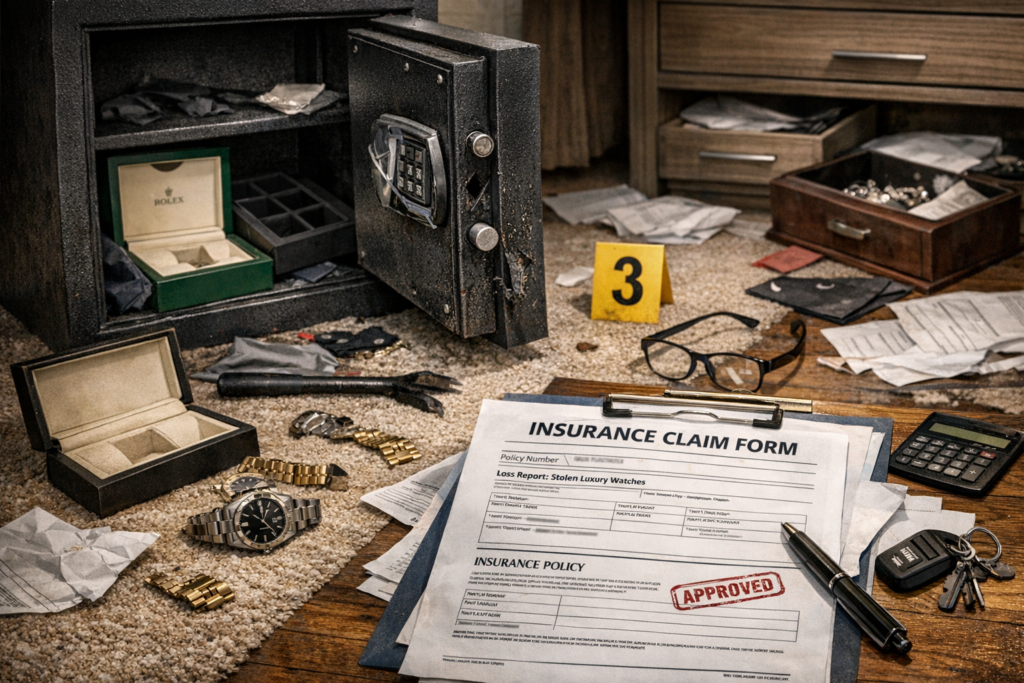

Many collectors assume the safest place for their watches is at home. Ironically, that’s where a large percentage of theft claims actually occur.

Whether insurance pays after a home theft depends on how the watch was stored, what policy you have, and whether exclusions apply. This guide explains what’s covered, what isn’t, and how to avoid denied claims.

Overview

Luxury watch insurance can cover theft at home, but homeowners insurance usually does not—at least not adequately. Understanding coverage terms before a loss occurs is critical.

Question: Does watch insurance cover theft at home?

Answer: Yes, luxury watch insurance typically covers theft at home when the policy includes all‑risk coverage. Homeowners insurance often has low limits and exclusions that result in partial or denied payouts.

Why Homeowners Insurance Often Fails at Home

Homeowners policies usually: • Cap jewelry coverage at $1,000–$5,000 total

• Apply high deductibles

• Require proof of forced entry

If your watch is stolen during a burglary, you may receive far less than its value—or nothing at all.

That’s why luxury watch insurance exists.

Common Home Theft Scenarios That Are Covered

Specialty insurance typically covers: • Break‑ins while you’re away

• Theft from a home safe

• Theft during forced entry

• Loss during disasters or evacuations

Coverage applies whether the watch was worn or stored—assuming reasonable precautions.

CTA 1

Compare insurance policies that include true all‑risk coverage for theft at home.

Storage and Security Matter

Insurers evaluate: • Whether a safe was used

• If the safe was anchored

• Alarm system presence

• Access control

Negligence—such as leaving watches unsecured—can complicate claims.

How Insurers Evaluate Home Theft Claims

Claims usually require: • Police report

• Proof of forced entry

• Appraisal or receipts

• Photos and serial numbers

According to U.S. insurance regulators, high‑value personal items often require separate scheduled coverage beyond standard homeowners policies.

For documentation guidance, see How to Appraise Your Watch for an Insurance Policy.

Choosing Coverage That Protects Against Home Theft

Home Watch Insurance Coverage Gap Checker

See how much of your watch’s value may be uninsured if it’s stolen at home.

Confirm your policy includes: • All‑risk theft coverage

• Agreed value payouts

• Reasonable storage requirements

To compare providers, review best luxury watch insurance options and analyses like Jewelers Mutual vs Hodinkee Insurance.

CTA 2

Get quotes from insurers that protect watches at home—not just on paper.

Quick Checklist: Preventing Home Theft Denials

• Use an anchored safe

• Install monitored alarms

• Limit access

• Document storage practices

• Keep appraisals current

Key Takeaways

Luxury watch insurance covers theft at home when written correctly.

Homeowners insurance usually leaves collectors underinsured.

CTA 3

Protect your watches at home with insurance built for high‑value assets—not household goods.

Next Read

• Is Homeowners Insurance Enough for a $10,000 Watch?

• How to Protect Expensive Watches