• How market changes affect insurance valuations

• When to update appraisals sooner than expected

• How outdated appraisals can reduce claim payouts

⚡ TL;DR: You should update your watch insurance appraisal every 1–3 years, or immediately after major market value changes, to avoid being underinsured if a claim occurs.

How the Watch Market Affects Insurance Appraisals

Intro

Many watch owners treat their initial insurance appraisal as a one‑time task. Once the paperwork is filed, it’s easy to assume coverage will remain adequate indefinitely. Unfortunately, luxury watch markets do not behave that way.

Prices can move rapidly based on demand shifts, brand decisions, and broader economic conditions. When appraisals lag behind reality, coverage gaps form quietly, often going unnoticed until a claim occurs.

CTA #

Understanding how frequently appraisals should be updated helps prevent insurance coverage from drifting out of sync with real‑world replacement costs.

Overview

Most insurers recommend updating watch appraisals every two to three years. This guideline works as a baseline, but it does not account for market volatility, category‑specific behavior, or sudden value changes.

Insurance coverage depends on replacement value, not purchase price. A deeper explanation of how coverage and valuation interact is outlined here: https://luxurywatchinsurance.net/luxury-watch-insurance-coverage-2/

Question: How often should a watch insurance appraisal be updated?

Answer: Most watches should be reappraised every two to three years, but high‑value, vintage, or volatile models may require annual updates depending on market conditions.

At‑a‑Glance Quick Answers

• Standard update cycle is every two to three years

• High‑value watches may need annual reviews

• Market spikes can require immediate reappraisal

• Under‑insurance reduces claim payouts

• Replacement value matters more than purchase price

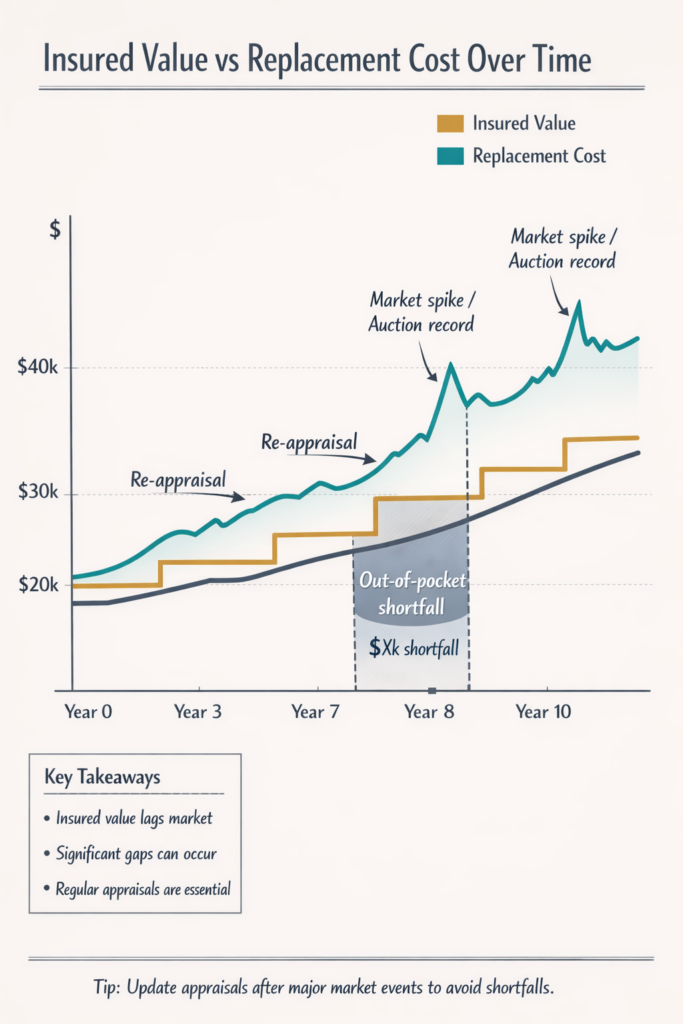

Why Outdated Appraisals Create Risk

When appraisals fall behind market value, under‑insurance becomes a serious issue. Policies often limit payouts to the insured amount, even if replacement costs have risen dramatically.

Some insurers also apply proportional settlement rules when significant under‑insurance exists, reducing payouts even for partial losses. The cost of updating an appraisal is minimal compared to the potential shortfall during a claim.

CTA #

Keeping appraisals current protects against silent coverage gaps that only surface when a loss occurs.

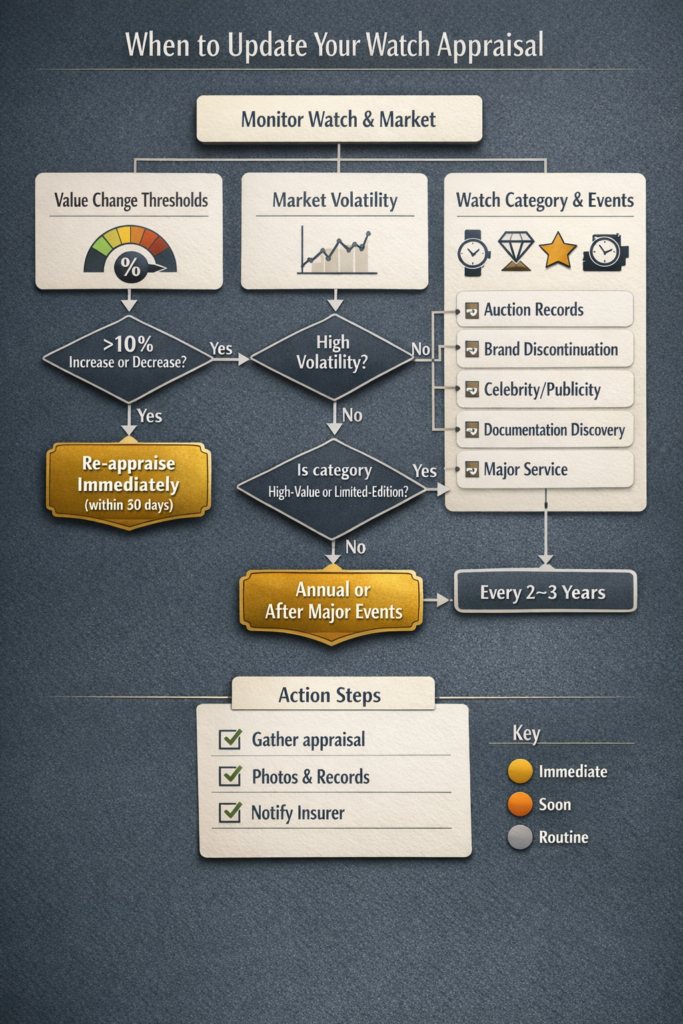

Market Triggers That Require Immediate Reappraisal

Certain events justify updating an appraisal immediately, regardless of when the last valuation occurred. Brand discontinuations, major auction results, celebrity exposure, and sudden demand shifts can all move prices quickly.

Discovering original boxes, papers, or service history can also increase value substantially. Any material change to a watch’s condition, originality, or documentation should prompt a fresh valuation.

How Different Watch Categories Behave

Modern luxury sports watches often experience sharp swings in secondary‑market pricing. For watches valued above roughly twenty to thirty thousand dollars, annual appraisal reviews may be appropriate.

Vintage watches behave differently. Their values depend heavily on condition, originality, and provenance. Subtle changes can significantly affect pricing, making two‑year appraisal cycles a safer ceiling.

Independent and microbrand watches require appraisers familiar with niche markets. Contemporary luxury watches with stable demand often tolerate longer appraisal intervals unless limited editions or discontinuations change demand.

CTA #

Matching appraisal frequency to watch category reduces unnecessary costs while keeping coverage aligned with market reality.

The Professional Appraisal Process

A professional appraisal involves authentication, condition assessment, and market research. Appraisers evaluate reference numbers, serials, originality, and recent comparable sales rather than advertised asking prices.

Reports include detailed photographs and descriptions that become essential evidence during claims. Replacement value, not fair market value, is the figure insurers use to determine coverage limits.

Building a Personal Appraisal Schedule

Creating a simple tracking system helps prevent oversight. Lower‑value watches often fit a three‑year cycle, mid‑range watches benefit from two‑year updates, and high‑value or volatile pieces warrant annual review.

Monitoring market movement between formal appraisals can help determine when an update is necessary without incurring unnecessary costs.

CTA #

A structured appraisal schedule removes guesswork and prevents coverage from quietly becoming inadequate.

How Insurers View Appraisal Updates

Specialist insurers understand market volatility and expect periodic appraisal updates. General homeowners policies often lag behind market realities and impose low sublimits.

Reviews of specialty insurers such as WonderCare and Hodinkee illustrate how appraisal‑based coverage is handled differently from standard homeowners policies: https://luxurywatchinsurance.net/wondercare-luxury-insurance-review/https://luxurywatchinsurance.net/hodinkee-watch-insurance-review-2/

A broader comparison of insurer approaches can be found here: https://luxurywatchinsurance.net/best-luxury-watch-insurance-2026/

When Market Corrections Occur

Market declines raise questions about whether to reduce coverage. Temporary corrections often reverse, while structural declines may justify adjusting insured values.

Insurers typically do not force reductions, but claims may be evaluated against current market conditions. Working with insurers experienced in collectibles helps manage this complexity.

Navigating Claims With Updated Appraisals

Current appraisals simplify claims by reducing disputes over value. Documentation, photographs, and valuation reports establish the insured position clearly.

For general consumer guidance on insurance claims and documentation standards, the National Association of Insurance Commissioners provides educational resources: https://www.naic.org/consumer_home.htm

FAQs

How much does a watch appraisal cost?

Most appraisals range from approximately $150 to $500 depending on complexity.

Does homeowners insurance cover luxury watches?

Coverage is usually limited unless watches are specifically scheduled with appraisals.

Can a receipt replace an appraisal?

Receipts may work for lower‑value watches, but higher‑value pieces typically require appraisals.

How long does an appraisal take?

Inspection takes under an hour, but reports usually take several days.

Should appraisals be updated if values fall?

Short‑term dips may not require changes, but permanent declines may justify adjustments.

Key Takeaways

• Two‑to‑three‑year cycles work for many watches

• High‑value or volatile watches may need annual updates

• Market events can trigger immediate reappraisal

• Under‑insurance significantly reduces claim payouts

• Appraisal costs are minor compared to potential losses

CTA #

Keeping appraisals current is one of the simplest ways to protect a watch collection from preventable insurance shortfalls.

Next Read

Luxury Watch Insurance Coverage Explained

https://luxurywatchinsurance.net/luxury-watch-insurance-coverage-2/

Best Luxury Watch Insurance in 2026

https://luxurywatchinsurance.net/best-luxury-watch-insurance-2026/