⚡ TL;DR: Homeowners insurance technically covers Cartier watches, but strict sublimits, deductibles, and exclusions mean most owners receive only a fraction of their watch’s true value—if anything at all.

READ ME

This article is for Cartier watch owners who assume their homeowners insurance protects high‑value pieces like the Tank, Santos, Ballon Bleu, or Panthère. It solves the problem of misunderstood coverage by explaining exactly how homeowners policies treat luxury watches and where the dangerous gaps exist. It supports affiliate revenue by guiding readers toward specialized watch insurance when homeowners coverage falls short. This article fits into the Cartier insurance cluster and funnels authority and trust back to the luxury watch insurance pillar page.

• What the article explains: How homeowners insurance actually covers (and limits) Cartier watches

• Why the reader should care: Most Cartier watches are dramatically underinsured without owners realizing it

• What decision it helps them make: Whether to rely on homeowners insurance, schedule a watch, or get specialized coverage

Intro

Have you ever stopped to think whether your homeowners insurance actually protects your Cartier watch? If you’re wearing a luxury timepiece worth tens of thousands of dollars, it’s easy to assume your standard policy has you covered.

The reality is far more complicated—and this is something many collectors only discover after a devastating loss. Homeowners insurance does offer some coverage for Cartier watches, but the protection is usually so limited that calling it real coverage feels misleading.

Understanding these limits before something happens is the difference between a manageable setback and a catastrophic financial loss.

Overview

Homeowners insurance treats Cartier watches as personal property, grouped together with everyday household items. Because jewelry and watches are high‑theft targets, insurers impose strict sublimits that rarely reflect modern luxury watch values.

At the same time, many policies apply deductibles, depreciation, and narrow definitions of covered losses. This creates a massive gap between what Cartier owners think is protected and what insurers actually pay.

To understand how this fits into the broader picture of luxury watch protection, it helps to start with the core guide:

https://luxurywatchinsurance.net/luxury-watch-insurance-coverage-2/

At‑a‑Glance Quick Answers

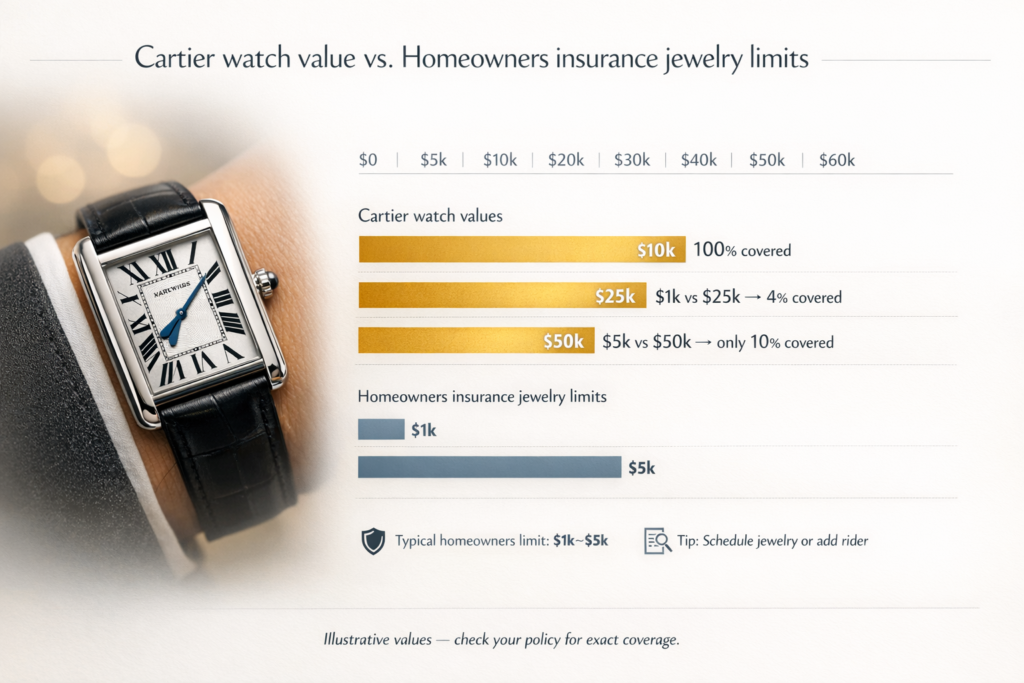

• Homeowners insurance usually caps Cartier coverage at $1,000–$5,000

• Deductibles further reduce payouts

• Loss and mysterious disappearance are usually excluded

• Coverage outside the home is often limited

• Specialized watch insurance fills these gaps

Main Sections

How Homeowners Insurance Treats Cartier Watches

Homeowners insurance divides coverage into categories, with personal property treated separately from your home itself. Jewelry and watches fall into a high‑risk category, so insurers apply sublimits regardless of your total coverage amount.

Most standard policies cap jewelry and watch coverage between $1,000 and $5,000 per item, and some cap all jewelry combined at $2,500 or $3,000.

For a $28,000 Cartier Santos, this means over 90% of the watch’s value may be completely uninsured.

What Is Actually Covered Under a Home Policy

If your Cartier is stolen during a confirmed burglary at your home, damaged in a house fire, or destroyed by a covered natural disaster, homeowners insurance may respond—up to the sublimit.

However, many policies pay jewelry claims at actual cash value, not replacement cost. That means depreciation applies, even if the watch has appreciated on the market.

Vintage Cartier Tanks and discontinued models are especially vulnerable here, as market value and insurer valuation often diverge sharply.

The Most Dangerous Coverage Gaps

Mysterious Disappearance

If your Cartier vanishes without clear evidence of theft—left in a hotel room, misplaced during travel, or simply gone—homeowners insurance typically denies the claim outright.

Accidental Damage

Drops, impacts, cracked crystals, and case damage are almost never covered unless tied to a named peril. Everyday accidents are excluded.

Travel and International Loss

Coverage often weakens or disappears entirely once the watch leaves your home, especially overseas. Theft from hotels and temporary residences is commonly limited or excluded.

These exclusions are where most Cartier owners discover too late that they weren’t protected at all.

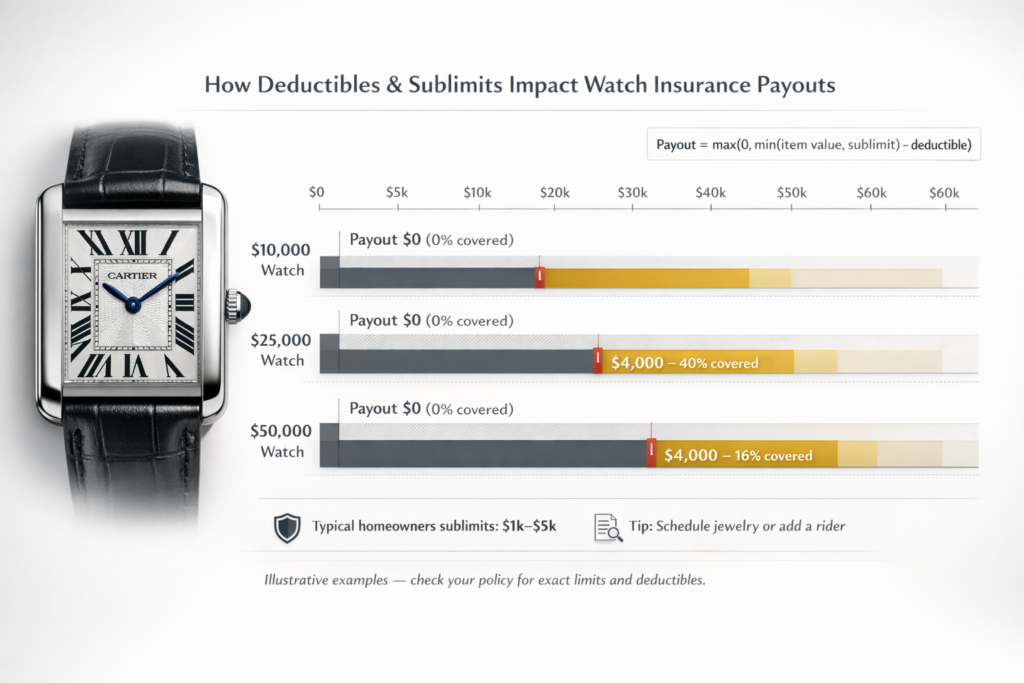

The Deductible Reality

Even when coverage applies, deductibles drastically reduce payouts.

Example:

An $8,000 Cartier Panthère is stolen.

• Jewelry sublimit: $2,000

• Deductible: $1,000

• Payout: $1,000

That’s a $7,000 loss—plus potential premium increases for years after filing the claim.

Scheduling a Cartier Watch on Homeowners Insurance

Some owners add a scheduled personal property endorsement to increase coverage limits.

Scheduling removes the sublimit and insures the watch for a specific value, usually based on an appraisal. Costs typically run 1%–2% of the watch’s value annually.

However, scheduling still has drawbacks: • Claims affect your homeowners insurance history

• Deductibles may still apply

• Coverage terms vary widely

• International and accidental coverage may remain limited

Scheduling is better than nothing—but still not equivalent to specialized watch insurance.

How Specialized Cartier Watch Insurance Differs

Specialized insurers design policies specifically for high‑value watches.

Typical features include: • All‑risk coverage

• Mysterious disappearance

• Accidental damage

• Worldwide protection

• Zero deductibles

• Agreed‑value payouts

Claims don’t affect your homeowners policy, and payouts reflect real market value.

For a step‑by‑step look at proper coverage, see:

https://luxurywatchinsurance.net/does-homeowners-insurance-cover-omega-watches/

(The same insurance mechanics apply across luxury brands.)

Real‑World Claim Scenarios

A Cartier Ballon Bleu stolen from a hotel safe overseas is often denied under homeowners insurance but fully covered under specialized watch insurance.

A cracked crystal from an accidental impact costs thousands to repair and is excluded by homeowners policies—but covered under all‑risk watch insurance.

A missing Cartier Tank with no clear explanation results in zero payout unless mysterious disappearance coverage exists.

These aren’t rare edge cases—they’re the most common losses collectors face.

Documentation That Matters

Regardless of policy type, insurers require documentation: • Purchase receipts

• Professional appraisals

• High‑resolution photographs

• Serial numbers

Appraisals should be updated every 1–3 years, especially as Cartier values fluctuate.

Cartier Watch Insurance Calculator

Estimate your insurance premium for luxury Cartier timepieces with comprehensive coverage options

Before deciding which route makes sense for your Cartier, the following tool helps estimate what proper coverage actually costs.

People Also Asked

Does homeowners insurance cover a lost Cartier watch?

Usually no. Mysterious disappearance is typically excluded.

How much does Cartier watch insurance cost?

Most specialized policies cost 1%–2% of the watch’s value annually.

Is accidental damage covered?

Not under homeowners insurance. Specialized policies usually cover it.

Can I insure a pre‑owned Cartier?

Yes, with a professional appraisal.

Key Takeaways

Homeowners insurance provides minimal protection for Cartier watches due to low sublimits, deductibles, depreciation, and exclusions. Scheduling a watch improves limits but still has drawbacks. Specialized watch insurance offers comprehensive, worldwide, agreed‑value coverage that aligns with how Cartier watches are actually used and valued.

CTA #

If your Cartier disappeared tonight, would your insurance replace it—or cap your payout at a fraction of its value? Now is the time to verify your coverage.

Next Read

Start with the foundation:

https://luxurywatchinsurance.net/luxury-watch-insurance-coverage-2/

Then continue with Cartier‑specific coverage:

https://luxurywatchinsurance.net/does-homeowners-insurance-cover-cartier-watches/