Why your Rolex needs more than homeowners coverage

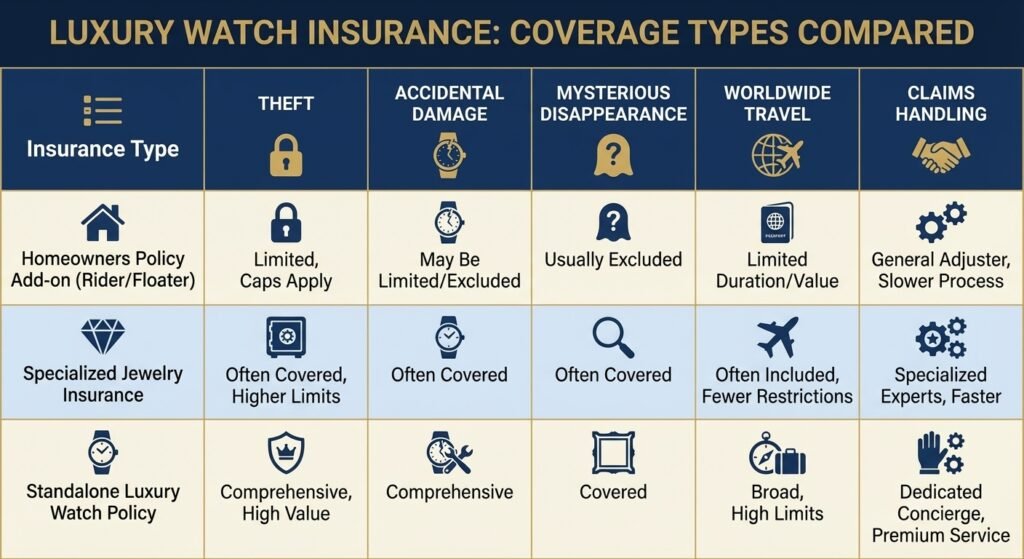

Standard homeowners insurance treats your $40,000 Patek Philippe like any other household item, which means you’re probably looking at a $1,000 to $2,000 payout cap per piece and zero coverage if your watch mysteriously disappears at an airport or gets damaged while traveling abroad.

Specialized luxury watch insurance exists to fix exactly that problem. The best providers offer worldwide all-risk coverage that protects against theft, loss, accidental damage, and mysterious disappearance, usually with no deductible and coverage that tracks with market appreciation.

If you own anything beyond a single entry-level luxury piece, or if you actually wear your watches instead of keeping them locked in a safe, dedicated watch insurance makes sense.

Below are the top providers in 2026, what they cover, what they cost, and who they work best for.

Top luxury watch insurance providers

CTA

>>Compare the top luxury watch insurance providers side by side to see which offers the best coverage and pricing for your collection.<<

1. BriteCo

BriteCo consistently ranks as the best overall specialist for watch insurance, especially if you want a fast, fully digital experience with transparent pricing.

You get all-risk worldwide coverage that includes theft, damage, loss, and mysterious disappearance. The online quote process takes about two minutes, and policies can bind instantly with no lengthy paperwork or calls to an agent.

Most policies come with zero deductible, and premiums typically run between 0.5% and 1.5% of the watch’s insured value per year.

BriteCo is designed around modern luxury brands including Rolex, Patek Philippe, Audemars Piguet, Vacheron Constantin, Omega, and Cartier. The platform works particularly well for collections of one to twenty watches, and you can add or remove items throughout the year as your collection changes.

Sample annual premiums from BriteCo:

- Rolex Submariner at $9,100 coverage: $103 to $161 per year

- Rolex GMT-Master II at $22,500: $254 to $397

- AP Royal Oak at $48,000: $542 to $847

- Patek Philippe Nautilus at $130,000: $1,468 to $2,293

Best for: US-based owners who want instant online coverage and clear pricing with no agent calls.

Get your rate: Start with a free BriteCo quote to see exactly what you’ll pay per watch in under two minutes.

2. Hodinkee Insurance (underwritten by Chubb)

Hodinkee Insurance brings Chubb’s high-net-worth expertise into a collector-friendly digital package, and it’s the best option if you own watches that are appreciating rapidly.

The standout feature is investment protection with coverage up to 150% of the insured value per watch, up to your total policy limit. That buffer matters when you insured a steel Daytona at $30,000 two years ago and it’s now trading at $45,000.

You also get all-risk, worldwide protection with no deductible on covered losses, and the setup is fast with photos and a short online flow that can go live in minutes if approved.

Hodinkee’s collector-focused approach means the platform understands the nuances of references, market movements, and why someone would wear a six-figure watch on a commercial flight.

Sample annual premiums from Hodinkee / Chubb:

- Omega Speedmaster at $5,350: $59 per year

- Rolex Submariner at $8,100: $89

- Cartier Tank Française at $19,100: $210

- AP Royal Oak at $25,800: $282

- Patek Philippe 5172G at $73,700: $689

Best for: Collections valued above $50,000 where appreciation tracking and high limits matter, and owners who want both a top-tier carrier and a watch-nerd friendly interface.

Compare rates: If you own many six-figure pieces or expect continued appreciation, get a Hodinkee Insurance quote to benchmark the 150% value protection feature.

3. Jewelers Mutual

Jewelers Mutual has insured jewelry and watches for over a century, and it remains one of the most reliable zero-deductible options available.

The company offers all-risk coverage for damage, loss, theft, and mysterious disappearance with worldwide protection for travelers. Many policies come with zero deductible, so there’s no out-of-pocket cost when a claim is paid.

For newer watches below certain value thresholds, Jewelers Mutual often waives the appraisal requirement, which speeds up the onboarding process significantly.

The long track record matters if you value institutional stability and straightforward claims handling over a flashy app interface.

Best for: Owners who prioritize an established specialist insurer with a century of jewelry and watch claims experience and want zero-deductible peace of mind.

4. WAX Insurance

WAX focuses on collectibles broadly, which makes it a strong choice if your luxury watches sit alongside fine art, rare wine, or other high-value items.

You can insure watches up to $100,000 per item with all-risk policies that include accidental damage. WAX offers replacement cost coverage up to 150% of the insured value in certain scenarios, and pricing starts around 1% of value for some categories.

The platform allows you to manage many asset classes under a single policy, which simplifies administration if you already track several types of collectibles.

Best for: People whose watch collection is part of a broader collectibles portfolio and who want consolidated coverage across many asset classes.

5. GemShield

GemShield is built for speed and simplicity, which makes it ideal when you walk out of an authorized dealer with a new purchase and need immediate coverage.

The all-risk policy covers loss, theft, disappearance, and damage with worldwide protection. The online quote process is fast, and you can insure newly purchased watches almost immediately without waiting for appraisals or long underwriting reviews.

Typical premiums run around 1% to 2% of the watch’s value.

The platform isn’t as feature-rich as BriteCo or Hodinkee, but if your priority is getting a new Rolex or Patek covered before it leaves your wrist, GemShield delivers exactly that.

Best for: New buyers who just completed a purchase and want coverage live within hours, and owners who value simplicity over custom policy structuring.

Instant coverage: Just bought a new Rolex or Patek? Lock in protection with a GemShield quote before your watch even leaves the house.

6. State Farm Personal Articles Floater

If you already use State Farm for home or auto insurance and want to consolidate everything with one carrier, the personal articles floater provides solid watch coverage within that ecosystem.

You get worldwide coverage with replacement cost terms and an optional deductible. Coverage amounts adjust automatically each year for inflation, and you can schedule many categories on the same floater, not just watches.

The main downside is that there’s no fully online quote process, so you’ll need to work with a local State Farm agent to set things up.

Best for: People who strongly prefer keeping all insurance with one major carrier and owners with modest watch values who want an incremental upgrade from basic homeowners coverage.

7. Chubb Masterpiece (Direct)

Beyond the Hodinkee consumer platform, Chubb itself remains the gold standard for insuring very high-value jewelry and watch collections through its direct private-client relationships.

You get highly flexible worldwide coverage with generous limits and typically no deductible for most jewelry and watch losses. Chubb offers tailored underwriting and risk-management guidance for large collections, and the service combines seamlessly if you already use Chubb for homes, yachts, fine art, or other high-net-worth needs.

This option makes sense when your watch collection is one component of a broader wealth protection strategy that needs white-glove service and deep customization.

Best for: Ultra-high-net-worth households with collections in the high six or seven figures who want a single private-client relationship covering all major assets.

How to choose the best luxury watch insurance

Watch Collection Insurance Calculator

Estimate your annual premium for insuring your timepiece collection

When you compare providers, focus on a few core variables that drive real differences in coverage and cost.

Coverage scope: All-risk policies are preferable to named-perils coverage because they protect against everything except specific exclusions. Confirm that mysterious disappearance is included by default and verify that worldwide travel protection has no territorial exclusions for countries you regularly visit.

>>Get real quotes from specialist luxury watch insurers to understand how coverage options and pricing compare for your specific watches.<<

According to U.S. insurance regulators, high‑value personal items often require separate scheduled coverage beyond standard homeowners policies.

Limits and valuation: Understand both the per-item limit and the total policy limit. Ask whether coverage is based on appraised value, purchase price, or current market value, and whether the policy offers up to 150% of insured value to account for appreciation.

Deductibles and premiums: Zero-deductible options increase predictability but may slightly raise premiums. Typical specialist watch insurance costs between 1% and 2% of value per year, though some providers offer lower averages.

Run quotes with identical watch lists and deductible structures to make accurate comparisons.

Claims process: Digital claims filing and tracking matters when something goes wrong. Check whether repairs go through authorized watchmakers and brand service centers, and research each provider’s reputation for fast payouts and clear communication.

Integration with your broader plan: For collections above six figures, think about how watch insurance fits alongside vault storage, home security systems, and estate planning. Some providers can coordinate with wealth managers or family offices to create a unified risk-management approach.

What to do before you buy

Before you bind a policy, document your collection thoroughly. Create a spreadsheet with brand, model, reference, serial number, purchase date, purchase price, and current estimated market value for each watch.

Collect supporting documents including invoices, authorized dealer receipts, auction records, original warranty cards, boxes, and service history.

Take photos from many angles with close-ups of serial numbers, which help both underwriting and future claims.

For pieces above certain thresholds, most insurers require professional appraisals. Work with a specialist watch appraiser who understands secondary-market pricing and refresh appraisals every three to five years, or sooner if a reference experiences a significant price spike.

Get quotes from at least two providers using identical watch lists and deductible structures. BriteCo or GemShield work well for an online specialist baseline, while Hodinkee Insurance or Jewelers Mutual provide strong collector-oriented comparisons.

Review exclusions carefully, looking for limits on unattended items in cars or hotel rooms, requirements for safes above certain value thresholds, and exclusions tied to professional use or extreme sports.

Action step: Complete your collection inventory this week, then send the same list to two top providers. Rate and coverage differences are often surprisingly large.

Common mistakes to avoid

The biggest mistake is assuming homeowners or renters insurance provides adequate protection. Standard policies typically cap jewelry coverage at $1,000 to $2,000 per item without a rider and often exclude mysterious disappearance and travel-related losses.

Relying on basic coverage alone usually leaves most of your watch’s value uninsured.

Another frequent error is failing to update insured values as the market moves. If you insured a Nautilus or specific steel sports reference at old retail figures, you could face a significant gap between the payout and actual replacement cost when prices spike.

Review your insured values at least annually and adjust coverage upward on high-momentum pieces.

Not disclosing key details creates claim friction later. Be upfront about where watches are stored, how often they’re worn while traveling, and whether pieces are ever used for commercial purposes.

Missing receipts, serial records, or photos slow down claims, so maintain a digital folder with documentation for each piece.

Finally, many collectors insure their first major watch at purchase but never update coverage as they build a collection. Treat insurance as part of your acquisition process, not an afterthought, and update your policy every time you buy or sell a watch.

My pick for 2026

BriteCo is the best starting point for most luxury watch owners. The combination of all-risk worldwide coverage, competitive pricing, zero deductible, and a genuinely fast digital experience makes it the easiest option to set up and manage.

You can get a real quote in two minutes, bind coverage instantly, and actually understand what you’re paying for without decoding insurance jargon or sitting through agent calls.

For larger collections or watches experiencing rapid appreciation, Hodinkee Insurance underwritten by Chubb offers more sophisticated protection. The 150% insured value feature creates a meaningful buffer when references spike, and the backing of Chubb’s high-net-worth infrastructure provides confidence for six-figure collections.

The platform understands collectors and feels purpose-built for people who actually wear serious watches instead of just vaulting them.

The key decision is to stop relying on inadequate homeowners coverage and move to a deliberate, itemized plan that matches how you actually live with your watches. When you do that, the annual premium becomes a small line item compared to the peace of mind you gain every time you leave home with a valuable watch on your wrist.

Take one evening this week to inventory your collection and pull quotes from BriteCo and Hodinkee.

Once proper coverage is in place, you can enjoy what you own instead of worrying about it.

Final step: Get quotes from at least two of the best luxury watch insurance providers this week. Compare coverage scope, limits, deductibles, and premiums side by side, then bind the policy that fits your collection and lifestyle.

Frequently asked questions

Is luxury watch insurance worth it for a single $10,000 watch?

Yes, dedicated watch insurance is worthwhile even for a single watch at that value. Standard homeowners policies typically pay only $1,000 to $2,000 without a rider and often exclude mysterious disappearance or travel losses.

Specialist policies usually cost 1% to 2% of value per year, which translates to $100 to $200 annually.

That’s a modest price to avoid a five-figure out-of-pocket replacement if something goes wrong.

Does watch insurance cover international travel and hotel stays?

Most of the best luxury watch insurance providers offer worldwide coverage that includes hotels and international travel. Policies from BriteCo, Hodinkee Insurance, Jewelers Mutual, and similar specialists protect your watches globally as long as you follow reasonable care requirements.

Always confirm any territorial exclusions or specific conditions around leaving watches unattended in hotel rooms or vehicles before you travel.

>>Take 10 minutes this week to get quotes from at least two of the best luxury watch insurance providers and lock in coverage that fits how you actually wear and travel with your watches.<<

Will my policy cover mysterious disappearance if a watch just goes missing?

Specialist policies are specifically designed to include mysterious disappearance, meaning the watch is gone with no clear explanation of how or when it disappeared. This is a major differentiator from basic riders and standard property policies, which often exclude this scenario. BriteCo, Hodinkee Insurance, Jewelers Mutual, and similar providers all cover mysterious disappearance by default.

How are vintage or discontinued watches valued for insurance purposes?

Insurers rely on professional appraisals that reflect current market value rather than original retail price. For highly traded references, appraisers reference recent auction results and dealer pricing to establish accurate values.

Some policies then add a cushion by paying up to 150% of the insured value if the market has moved significantly since the last appraisal, which helps protect against rapid appreciation.

Does insurance cover scratches and normal wear and tear?

Fine scratches and normal cosmetic wear typically fall under maintenance rather than covered damage. However, accidental damage such as a cracked crystal from a drop, significant impact damage, or water infiltration beyond the watch’s rated depth is generally covered under all-risk policies.

Read your specific policy wording or ask your provider how they define “accidental damage” versus “wear and tear.”

Can I insure watches kept in a bank vault at a lower premium?

Some insurers offer preferential rates for watches stored primarily in bank vaults or high-security home safes compared with pieces worn daily. The risk profile is lower for vaulted watches, so you may be able to negotiate better terms or higher deductibles on rarely worn pieces to improve your overall premium.

Discuss storage locations and wearing frequency with providers when requesting quotes.

What happens if I sell or trade a watch that’s now insured?

Update your policy immediately when a watch leaves your possession. Most providers let you add and remove items mid-term with premium adjustments.

If you forget to remove a sold watch, you’ll continue paying for coverage you no longer need, and outdated records can complicate future claims if insurers explore discrepancies during the claims process.

References:

BriteCo, “Watch Insurance”

Benzinga, “Best Watch Insurance Providers”

Hodinkee Insurance, “All-Risk Watch Insurance underwritten by Chubb”

WPB Watch Co., “Luxury Watch Insurance – How to Protect Your Investment”

Jewelers Mutual, “Watch Insurance”

Chubb, “Insurance for Jewelry, Watches, Rings & More”