⚡ TL;DR: Cartier warranties cover rare manufacturing defects, while watch insurance covers the real risks—loss, theft, damage—so understanding the difference is the key to protecting your watch properly.

READ ME

This article is for Cartier watch owners who want to clearly understand the difference between Cartier’s warranty and dedicated watch insurance. It solves the problem of false security by breaking down exactly what each option protects—and what they explicitly exclude. It supports affiliate revenue by educating readers on why warranty alone is insufficient and when specialized insurance becomes necessary. This article sits mid‑to‑late funnel in the Cartier cluster and reinforces authority from the luxury watch insurance pillar.

• What the article explains: What Cartier warranties protect vs what watch insurance actually covers

• Why the reader should care: Most real‑world losses fall outside warranty protection

• What decision it helps them make: Whether to rely on warranty, insurance, or both

Intro

When you invest in a Cartier watch, you’re making a serious financial commitment—often $5,000 to $50,000 or more. Naturally, you want that investment protected.

Most Cartier owners believe they’re covered simply because they registered their watch and received an official warranty card. Unfortunately, that confidence disappears the moment something actually goes wrong.

If your watch is stolen while traveling, dropped onto a hard surface, or mysteriously disappears from a hotel room, you’ll quickly learn that warranty protection and real‑world protection are not the same thing.

Overview

Cartier owners usually rely on three perceived layers of protection: the manufacturer warranty, homeowners insurance, and sometimes specialized watch insurance. Each of these protects very different risks—and excludes most others.

Understanding how these protections differ is essential if you want to avoid discovering coverage gaps after a loss. For a complete foundation on luxury watch insurance, start here:

https://luxurywatchinsurance.net/luxury-watch-insurance-coverage-2/

At‑a‑Glance Quick Answers

• Cartier warranty covers defects only

• Insurance covers theft, loss, and damage

• Home insurance caps jewelry payouts

• Warranty extensions don’t expand coverage

• Insurance protects real‑world risks

Main Sections

What Cartier’s Warranty Actually Covers

Cartier provides a standard 24‑month international warranty starting from the date of purchase. This warranty covers manufacturing defects—nothing more.

If a component fails because it was improperly made or assembled, Cartier will repair or replace it at no cost during the warranty period. That protection has value, but it applies to a very narrow set of circumstances.

Manufacturing defects account for a small percentage of real‑world watch problems. Most damage comes from daily wear, travel, impacts, or loss—all excluded under warranty terms.

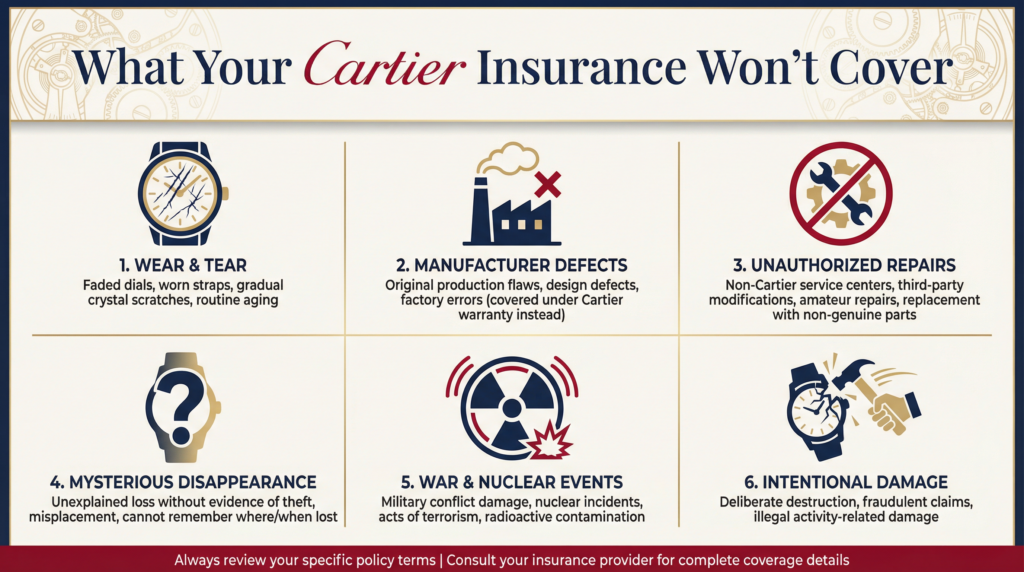

Excluded under warranty: • Accidental damage

• Theft or loss

• Water damage

• Normal wear and tear

• Scratches or dents

• Unauthorized repairs

Cartier Care Warranty Extension: What Changes (and What Doesn’t)

Cartier Care extends the same manufacturing‑defect coverage from 2 years up to a maximum of 8 years if registered within the first 24 months.

What it does: • Extends defect coverage timeline

What it does not do: • Add theft protection

• Cover accidental damage

• Cover loss or mysterious disappearance

The extension is free and worth registering—but it does not replace insurance.

What Specialized Cartier Watch Insurance Covers

Dedicated watch insurance exists specifically to protect against scenarios warranty excludes.

Typical coverage includes: • Theft (home or travel)

• Accidental damage

• Loss

• Mysterious disappearance

• Sudden physical damage

For a $20,000 Cartier watch, insurance typically costs $200–$1,000 per year (1–5% of value). That premium often equals less than the cost of a single out‑of‑warranty repair.

Insurance follows the watch worldwide and usually offers zero‑deductible or low‑deductible claims.

The Homeowners Insurance Illusion

Homeowners and renters insurance technically includes jewelry—but with strict sublimits.

Most policies cap jewelry payouts between $2,000 and $5,000 total, regardless of the watch’s true value. Deductibles further reduce payouts.

Excluded scenarios often include: • Accidental damage

• Mysterious disappearance

• Theft while traveling

Scheduling a watch can improve limits, but coverage remains weaker than specialized insurance and claims can raise homeowners premiums.

The Water‑Resistance Warranty Paradox

Water resistance does not equal water‑damage coverage.

Every time a Cartier case is opened for service, water‑resistance coverage is void until pressure testing is performed. If testing isn’t documented and water enters the case later, warranty claims are denied.

Most owners are never told this.

Insurance, by contrast, typically covers sudden water damage regardless of service history.

Serial Numbers and Warranty Vulnerability

If your Cartier serial number becomes illegible—even from natural wear—warranty coverage ends permanently.

Insurance does not rely on physical serial visibility alone. Ownership can be proven through documentation, appraisals, and photographs.

This difference alone makes insurance more resilient than warranty for long‑term ownership.

Real‑World Scenarios: Warranty vs Insurance

Crystal cracked from impact

• Warranty: Not covered

• Insurance: Covered

Watch stolen from hotel

• Warranty: Not covered

• Insurance: Covered

Movement defect in year four

• Warranty (with extension): Covered

• Insurance: Not covered

Mysterious disappearance

• Warranty: Not covered

• Insurance: Covered

Building the Right Protection Strategy

The most effective strategy combines both tools.

• Register for Cartier Care within 24 months

• Purchase specialized watch insurance

• Keep documentation updated

• Re‑appraise every 2–3 years

Warranty protects against unlikely factory defects. Insurance protects against likely real‑world losses.

Before reviewing common questions, the following tool helps evaluate whether your Cartier is properly protected.

Cartier Watch Coverage Exclusion Checker

Determine which warranty, homeowners insurance, and specialty insurance exclusions may affect your Cartier watch claim. This tool helps you understand coverage limitations and exclusions before filing a claim.

Widget Section #

Widget Needed: YES

Widget Title: Cartier Watch Protection Checker

Widget Prompt: Evaluate whether your Cartier watch is fully protected by warranty, insurance, or both.

People Also Asked

Does Cartier warranty cover scratches?

No. Scratches are considered normal wear and tear.

Is Cartier insurance worth it?

Yes for most watches over $3,000–$5,000.

Can I insure a pre‑owned Cartier?

Yes, with proper appraisal and authentication.

Does homeowners insurance cover Cartier watches?

Only minimally and often inadequately.

Key Takeaways

Cartier warranties cover only manufacturing defects and exclude nearly all real‑world risks. Specialized watch insurance fills these gaps by covering theft, loss, accidental damage, and mysterious disappearance. Homeowners insurance offers limited and often misleading protection. The most effective approach combines free warranty extension with dedicated watch insurance to fully protect your investment.

CTA #

If your Cartier were damaged or stolen tomorrow, would your warranty actually help—or leave you paying out of pocket? Now is the time to verify your protection.

Next Read

Start with the foundation:

https://luxurywatchinsurance.net/luxury-watch-insurance-coverage-2/

Then continue with Cartier‑specific coverage:

https://luxurywatchinsurance.net/does-homeowners-insurance-cover-cartier-watches/