• What it actually costs to insure an Audemars Piguet watch

• Why premiums vary so widely between owners

• How appreciation, location, and policy structure affect cost

⚡ TL;DR: Insuring an Audemars Piguet typically costs 1–2% annually but prevents catastrophic losses from theft or damage.

How Audemars Piguet Insurance Pricing Really Works

[IMAGE 1 – FEATURED]

ALT text: Audemars Piguet Royal Oak resting beside insurance documents

Intro

Audemars Piguet watches sit at the intersection of luxury, collectability, and financial risk. Owners often focus on purchase price but underestimate the long‑term cost of protecting a watch that may be worth tens or hundreds of thousands of dollars.

Insurance pricing for Audemars Piguet watches is not straightforward. Premiums vary widely based on value, geography, security measures, claims history, and policy structure. Advertised percentages rarely tell the full story.

Understanding how insurers calculate cost helps owners avoid both overpaying and underinsuring.

CTA #

Knowing how insurance costs are calculated prevents surprise expenses later.

Overview

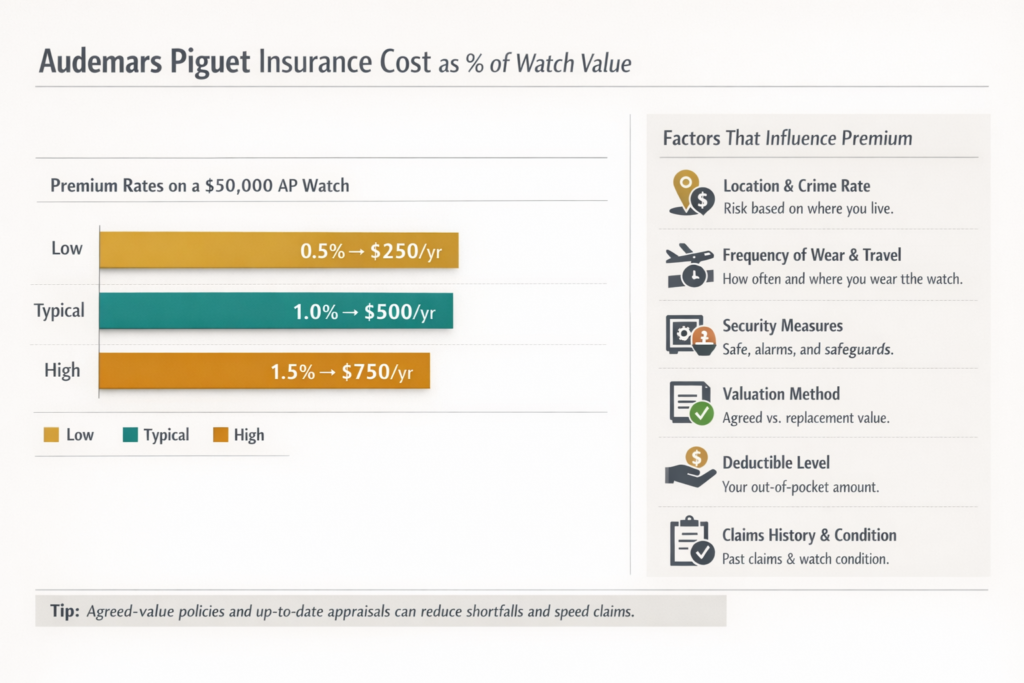

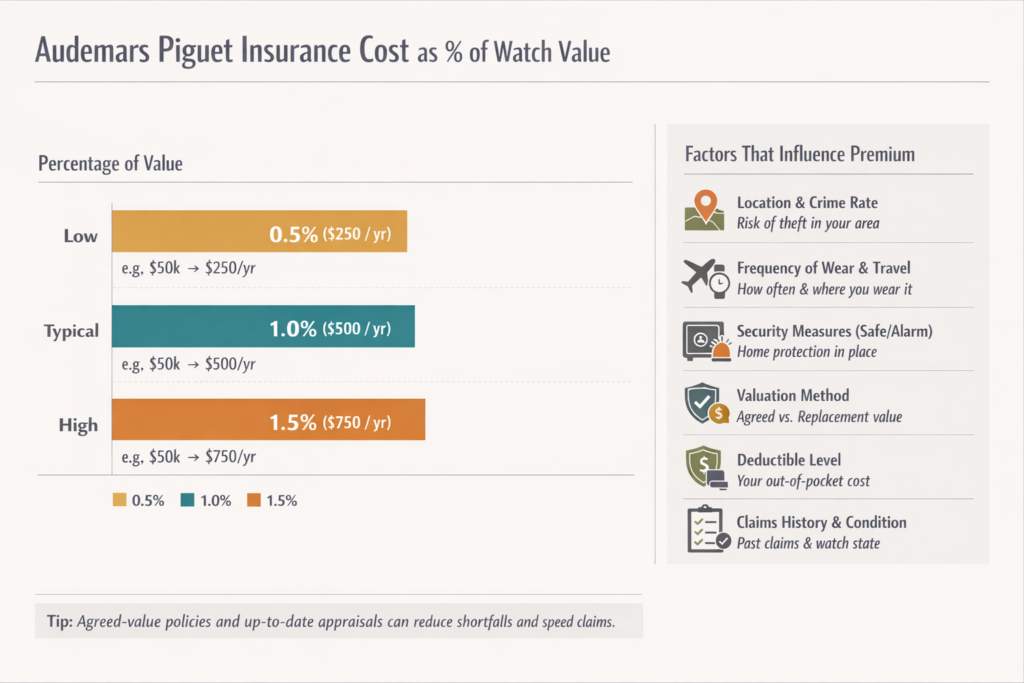

Most Audemars Piguet insurance policies price coverage as a percentage of the watch’s insured value. Typical ranges fall between 1% and 5% annually, depending on risk factors.

Specialty watch insurance usually clusters toward the lower end of that range, while single‑item or high‑risk policies trend higher.

A broader explanation of luxury watch insurance fundamentals is available here:

https://luxurywatchinsurance.net/luxury-watch-insurance-coverage-2/

Question: How much does it cost to insure an Audemars Piguet watch?

Answer: Insurance typically costs 1%–5% of an Audemars Piguet’s insured value annually, depending on location, security, and policy terms.

At‑a‑Glance Quick Answers

• Premiums are percentage‑based

• Higher values increase cost proportionally

• Location affects pricing significantly

• Deductibles reduce annual premiums

• Appreciation increases long‑term costs

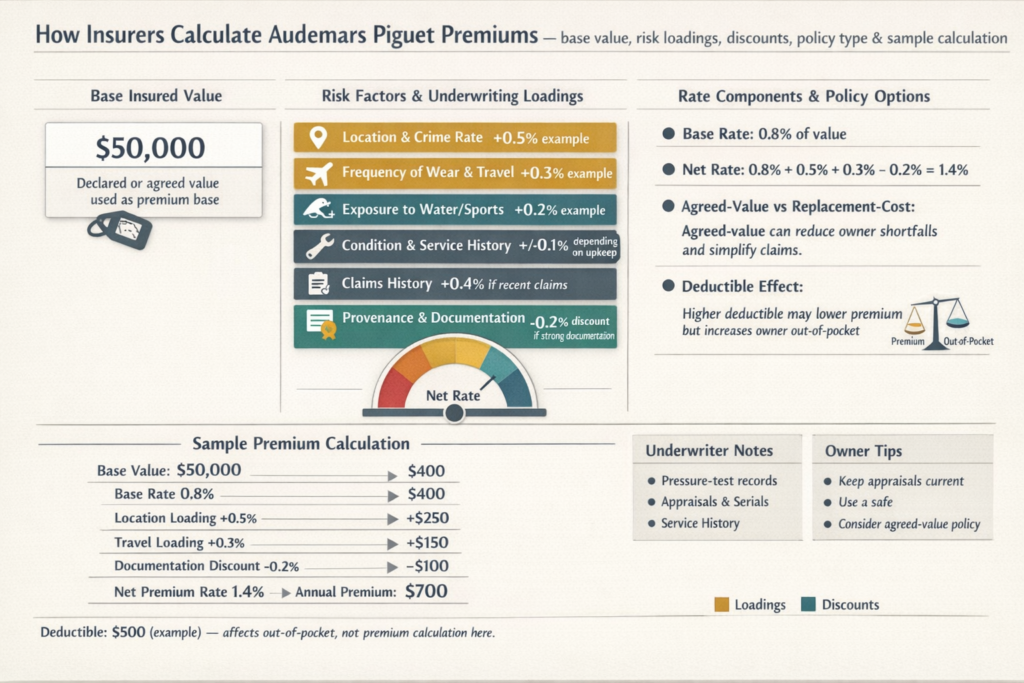

Base Premium Structure

Insurers calculate premiums as a percentage of insured value. A $30,000 Audemars Piguet typically costs $300–$600 annually under standard specialty coverage.

Higher‑risk scenarios, such as single‑watch policies, zero deductibles, or high‑crime locations, can push premiums toward 3%–5%.

This pricing reflects both theft risk and claim severity rather than manufacturing quality.

CTA #

Percentage pricing means insurance costs rise as watch values rise.

Geographic Pricing Differences

Location is one of the largest cost drivers. Urban areas with higher theft rates command higher premiums than suburban or rural locations.

Postcode‑based pricing in markets like the UK can create 30%–50% differences for identical watches owned by identical individuals in different neighborhoods.

Some insurers may decline coverage entirely in high‑risk locations, forcing owners into surplus or specialty markets with higher pricing.

Home Security and Discounts

Security measures influence both insurability and cost. Insurers often offer discounts for:

• Rated safes

• Alarm systems

• Secure anchoring

• Monitored security services

For high‑value AP watches, certain security measures may be mandatory rather than optional.

Upfront investment in security can reduce long‑term insurance costs.

CTA #

Security investment often pays for itself through lower premiums.

Deductibles and Their Impact

Deductible choices dramatically affect annual premiums. Zero‑deductible policies typically cost 20%–30% more than policies with $500–$1,000 deductibles.

Many collectors choose moderate deductibles to balance premium savings against out‑of‑pocket exposure.

Low deductibles also reduce claim hesitation when damage costs approach deductible thresholds.

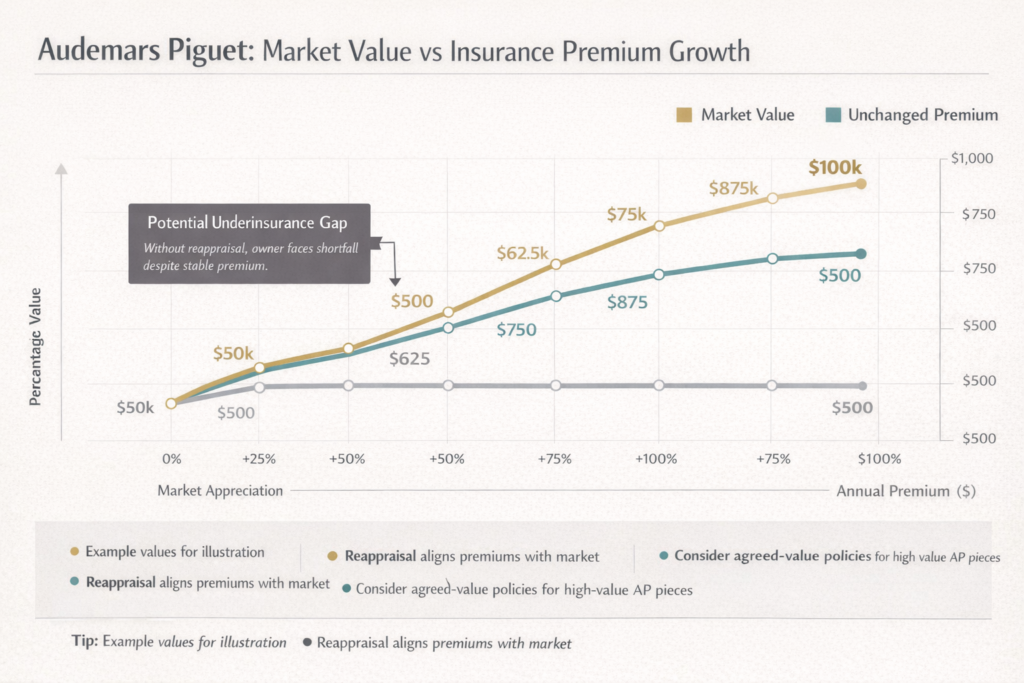

Market Appreciation and Revaluation Costs

Audemars Piguet watches often appreciate significantly. As insured value increases, premiums rise proportionally.

Owners must update appraisals every one to three years to maintain accurate coverage. Appraisal costs add $100–$300 per update, increasing total ownership cost.

Operating with outdated valuations leaves owners underinsured during claims.

Some insurers offer buffers or extended replacement provisions to mitigate appreciation risk.

CTA #

Appreciation increases both protection needs and insurance costs.

AP Coverage Service and Cost Implications

Audemars Piguet offers a complimentary coverage service for eligible purchases within specific date ranges. This service provides temporary protection against burglary, robbery, and functional damage.

Activation is required, coverage is time‑limited, and benefits do not transfer to new owners.

The service reduces short‑term insurance cost but does not replace long‑term coverage needs.

After the coverage period ends, owners must secure paid insurance to maintain protection.

Specialty Insurance vs Riders

Scheduling an AP on homeowners insurance may appear cheaper initially, but riders often include:

• Higher deductibles

• Narrow coverage

• Claims impacting homeowners policies

Standalone specialty watch insurance typically provides broader coverage and isolates claims from home insurance.

Insurers experienced with AP coverage include:

https://luxurywatchinsurance.net/wondercare-luxury-insurance-review/

https://luxurywatchinsurance.net/hodinkee-watch-insurance-review-2/

Audemars Piguet Insurance Cost Estimator

Calculate the estimated annual insurance premium for your luxury Audemars Piguet timepiece. Get personalized coverage recommendations based on your watch model, value, location, and security measures.

- Consider agreed value coverage to lock in your watch’s current market value

- Add worldwide coverage if you travel internationally with your timepiece

- Document your watch with professional appraisal and photographs

- Review coverage annually as AP values can appreciate significantly

CTA #

Comparing policy structure matters more than comparing base premiums.

Claims History and Long‑Term Cost

Previous claims affect future premiums across insurers. Even paid claims create long‑term pricing consequences.

Some owners choose to absorb moderate losses rather than file claims that increase future costs.

Standalone policies reduce the impact on homeowners insurance history.

People Also Asked

How much does AP insurance cost per year?

Typically 1%–5% of insured value annually.

Does free AP coverage replace insurance?

No, it is temporary and limited in scope.

Are premiums tax deductible?

Usually not for personal property.

Does location really matter?

Yes, significantly.

Do collection policies reduce cost?

Yes, per‑item cost often decreases.

Key Takeaways

• AP insurance costs scale with value

• Location strongly affects pricing

• Security measures reduce premiums

• Appreciation increases long‑term cost

• Specialty insurance offers clearer value

CTA #

Understanding cost drivers helps owners choose insurance that fits both risk and budget.

Next Read

Luxury Watch Insurance Coverage Explained

https://luxurywatchinsurance.net/luxury-watch-insurance-coverage-2/

Best Luxury Watch Insurance in 2026

https://luxurywatchinsurance.net/best-luxury-watch-insurance-2026/