What qualifies as accidental damage for luxury watches

• What specialized watch insurance covers that homeowners policies do not

• How claims and repairs are handled after an accident

⚡ TL;DR: Luxury watch insurance usually covers accidental damage like drops, impacts, and cracked crystals, while homeowners insurance and manufacturer warranties typically do not.

How Accidental Damage Is Defined for Luxury Watches

Intro

Many watch owners assume insurance is insurance, and that any damage will be covered regardless of the policy. With luxury watches, that assumption often proves costly.

Drops, impacts, water exposure, and cosmetic damage regularly result in repair bills reaching into the thousands. Standard homeowners policies frequently exclude accidental damage or apply low jewelry limits, leaving owners unexpectedly exposed.

Specialized luxury watch insurance exists specifically to address these scenarios, covering sudden and unintended damage that occurs during normal wear and everyday life.

CTA #

Understanding how accidental damage is defined before an incident occurs helps prevent costly surprises later.

Overview

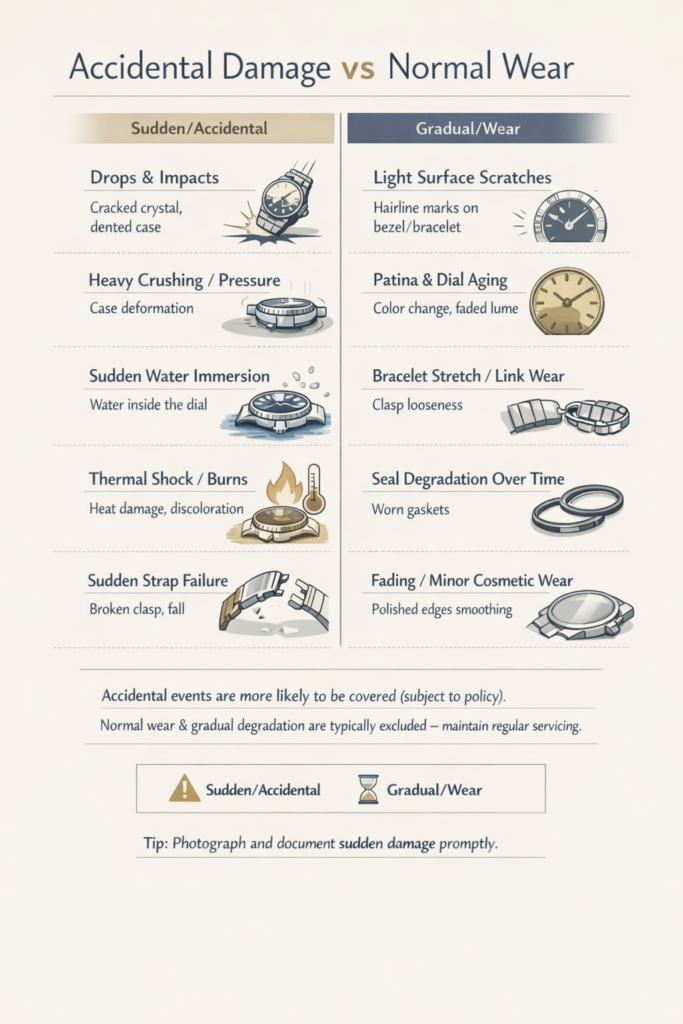

Accidental damage in insurance terms refers to sudden, unintended physical harm caused by a specific event. This definition separates covered accidents from excluded wear, aging, or maintenance issues.

Luxury watch insurance policies are structured around this distinction and typically operate on an all‑risk basis, covering most forms of accidental damage unless explicitly excluded. A detailed explanation of how coverage works is outlined here: https://luxurywatchinsurance.net/luxury-watch-insurance-coverage-2/

Question: Does luxury watch insurance cover accidental damage?

Answer: Yes. Most specialty luxury watch insurance policies cover accidental damage caused by sudden, unintended events such as drops, impacts, or water exposure, subject to policy terms.

At‑a‑Glance Quick Answers

• Drops and impacts are typically covered

• Accidental water damage is usually covered

• Cosmetic damage may be covered if sudden

• Wear and tear is not covered

• Coverage terms depend on policy wording

What Specialized Watch Insurance Covers

Specialized watch insurance anticipates the types of accidents that commonly occur with high‑value timepieces.

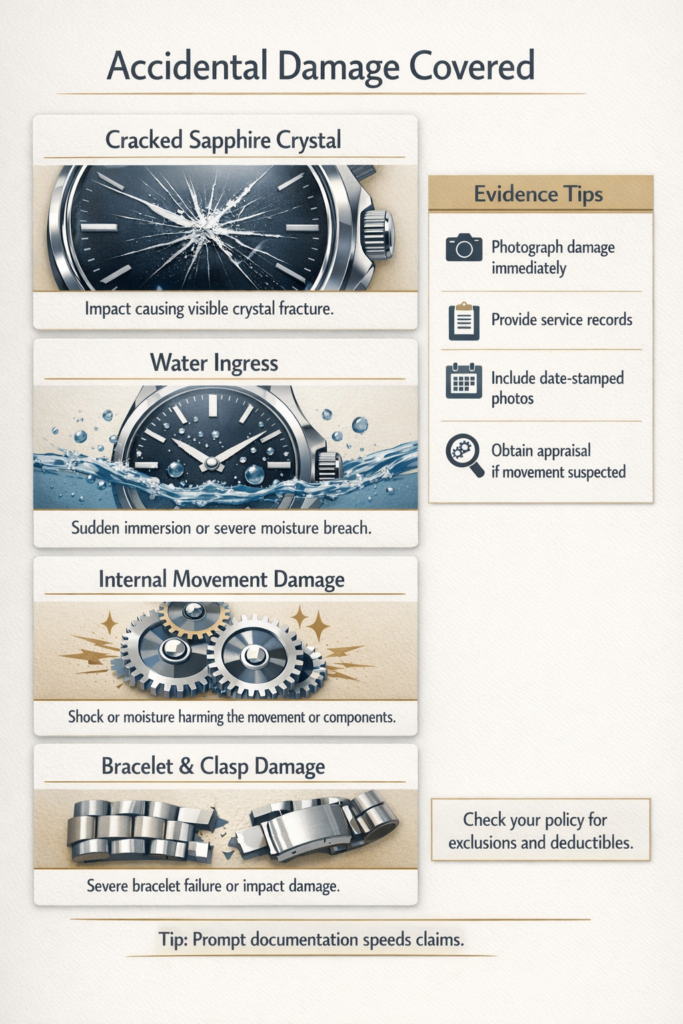

Crystal and glass damage is among the most frequent claims. Cracked or shattered sapphire crystals are covered, including labor, pressure testing, and resealing.

Water damage is also commonly covered when it results from accidents such as unsecured crowns or gasket failure. Policies typically pay for complete movement disassembly, cleaning, part replacement, and resealing.

Impact damage to internal components is another major coverage area. Hard knocks can damage balance wheels, jewels, or pivots even when external damage is minimal. These repairs are included under most specialty policies.

Cosmetic damage often distinguishes watch‑specific insurance from general policies. Dents, deep scratches, bezel damage, and case deformation may be covered when caused by an accident, including professional refinishing or restoration.

Bracelet and clasp damage is also covered, including bent links or damaged clasps that require replacement or specialized labor.

CTA #

Accidental damage coverage is designed for real‑world wear, not just catastrophic loss.

Key Exclusions to Understand

While coverage is broad, exclusions matter.

Normal wear and tear is not covered. Bracelet stretch, lubricant breakdown, fading lume, and routine servicing needs are considered maintenance.

Mechanical breakdown due to age or lack of servicing is excluded. Insurance does not replace routine maintenance.

Patina, gradual corrosion, and aging are excluded even if they affect appearance or value.

Intentional damage or knowingly risky behavior, such as exposing a non‑water‑resistant watch to swimming, may void coverage.

Manufacturing defects are typically handled under manufacturer warranties rather than insurance policies.

How Specialized Insurance Differs From Homeowners Policies

Homeowners insurance treats luxury watches as generic jewelry and often caps coverage between $1,000 and $5,000 per item.

Specialized watch insurance removes these caps, covering the full appraised value. Many policies offer zero‑deductible options and worldwide coverage.

Homeowners policies may exclude accidental damage entirely or restrict it heavily. Specialty policies operate on an all‑risk basis, covering most accidental events by default.

Repair handling also differs. Specialty insurers work with authorized service centers and qualified watchmakers to preserve value and warranty integrity.

Providers such as WonderCare and Hodinkee outline how watch‑specific coverage differs from homeowners insurance:https://luxurywatchinsurance.net/wondercare-luxury-insurance-review/ https://luxurywatchinsurance.net/hodinkee-watch-insurance-review-2/

CTA #

Choosing insurance designed specifically for watches reduces claim friction and repair disputes.

Filing Claims After Accidental Damage

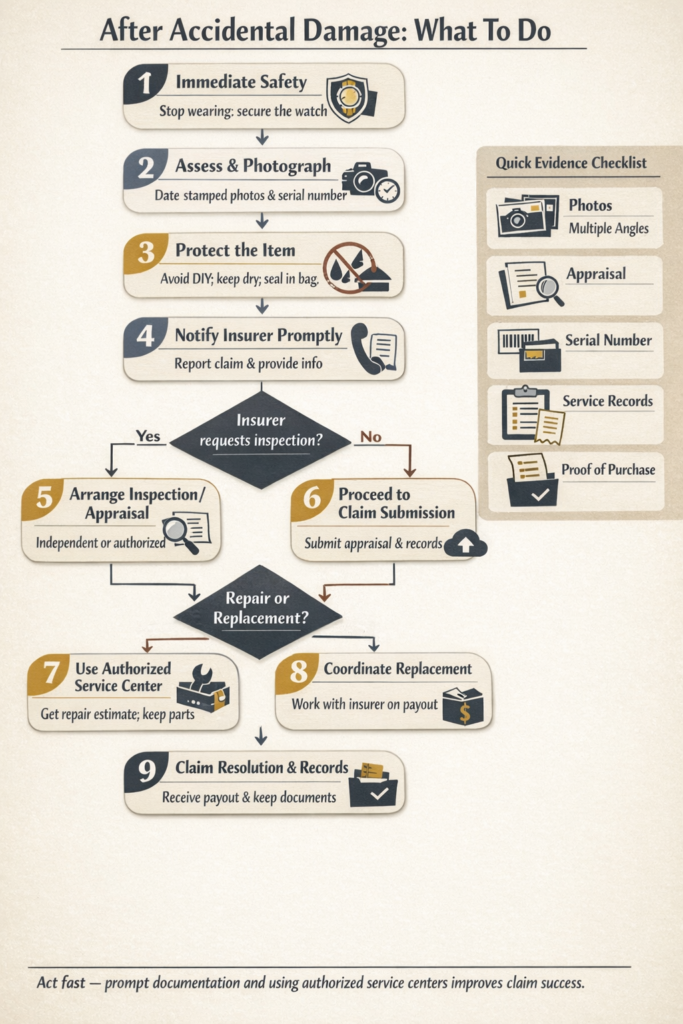

Claims typically begin with photographs, documentation, and a description of the incident. Insurers may coordinate directly with authorized service centers or request estimates depending on the damage.

Minor repairs may be approved quickly, while complex restorations can require detailed evaluation. Turnaround times vary based on parts availability and service center workload.

For general consumer guidance on insurance claims rights and documentation standards, reference materials are available from the National Association of Insurance Commissioners: https://www.naic.org/consumer_home.htm

[IMAGE 5 – COMPARISON]

ALT text: Comparison chart showing homeowners insurance versus specialty watch insurance coverage

Choosing the Right Coverage Level

Coverage should reflect current replacement value rather than purchase price. Regular appraisals, typically every two to three years, help keep coverage aligned with market values.

Agreed value policies offer the most certainty by eliminating valuation disputes at claim time. Premiums generally range from 1% to 3% of insured value annually.

A broader comparison of insurers and coverage approaches can be found here: https://luxurywatchinsurance.net/best-luxury-watch-insurance-2026/

CTA #

Coverage levels should be reviewed periodically to prevent under‑insurance during claims.

Preventing Accidental Damage

Removing watches during high‑risk activities, using protective storage, checking crowns before water exposure, staying current with servicing, and using travel cases can reduce accident risk.

FAQs

Does luxury watch insurance cover scratches?

Yes, accidental scratches and cosmetic damage may be covered if caused by a sudden event. Normal wear scratches are typically excluded.

Does watch insurance cover water damage?

Accidental water damage is usually covered, while gradual corrosion is excluded.

Can used watches be insured?

Yes. A current appraisal establishes value regardless of original purchase source.

Does homeowners insurance cover accidental damage?

Often no. Homeowners policies may exclude accidental damage or apply low sublimits.

What is agreed value coverage?

Agreed value coverage sets the payout amount in advance, eliminating depreciation disputes.

Key Takeaways

• Luxury watch insurance typically covers accidental damage

• Sudden events are covered; gradual wear is excluded

• Specialty policies differ significantly from homeowners insurance

• Repairs are handled by qualified service centers

• Regular appraisals help maintain proper coverage

CTA #

Accidental damage coverage is most effective when policy terms, valuation, and repair processes are clearly understood in advance.

Next Read #

Luxury Watch Insurance Coverage Explained

https://luxurywatchinsurance.net/luxury-watch-insurance-coverage-2/

Best Luxury Watch Insurance in 2026

https://luxurywatchinsurance.net/best-luxury-watch-insurance-2026/