• Learn what Hodinkee Insurance actually covers—and where it falls short

• Understand real‑world claims and customer service experiences

• Decide if Hodinkee is right for your watch collection and travel habits

Traveling internationally with your watch collection? Most standard insurance policies abandon you completely the moment you cross state lines, let alone international borders.

That’s exactly why I decided to investigate Hodinkee Insurance beyond the marketing hype and glossy website promises. I wanted to understand whether this platform actually solves genuine problems collectors face, or if it’s just another insurance product pretending to understand watch enthusiasts.

What I uncovered surprised me in both directions. There are genuinely innovative features that address real collector pain points, but there are also some concerning customer service patterns you absolutely need to know about before committing your collection to their coverage.

Why Traditional Insurance Fails Watch Collectors

Before getting into Hodinkee’s offering, it’s important to understand why standard homeowners and renters insurance creates massive coverage gaps for anyone with a serious watch collection.

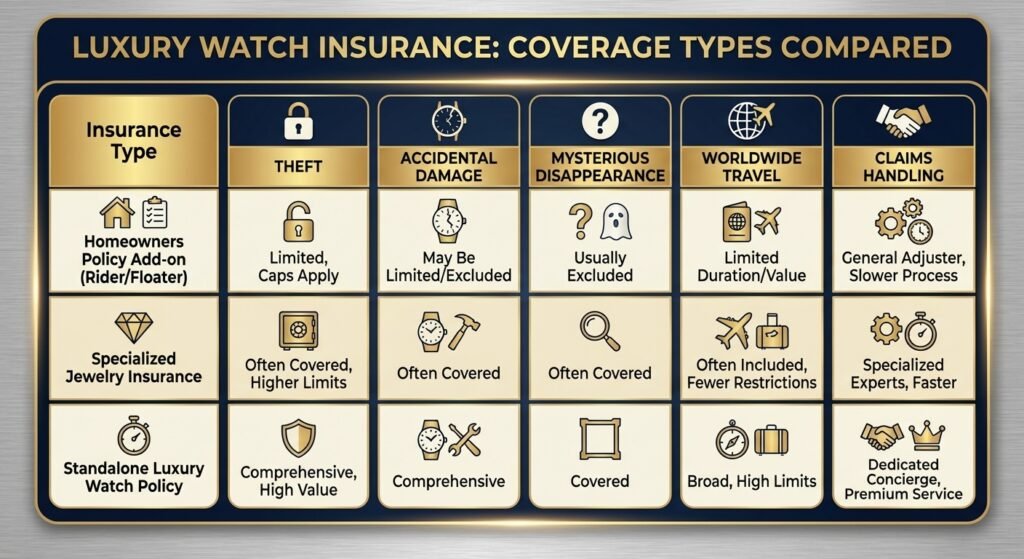

Most policies lump watches and jewelry into a single category with aggregate limits between $1,500 and $5,000. That means if someone steals multiple valuable watches, you may only receive a few thousand dollars total.

Even worse, these policies typically exclude mysterious disappearance. If your watch slips off your wrist or goes missing without clear evidence of theft, claims are often denied.

International travel is another major gap. Many policies void coverage outside your home country unless items are specifically scheduled, leaving collectors unknowingly uninsured during travel.

The Hodinkee Approach: What’s Actually Different

Hodinkee partnered with Chubb, a long‑established insurer with deep financial backing. This partnership ensures claims are supported by a major carrier rather than a small underwriter.

Hodinkee eliminates deductibles entirely. If you lose a watch, you receive the insured amount without paying anything out of pocket.

Coverage is worldwide and all‑risk by default, including theft, accidental damage, and mysterious disappearance.

One standout feature is self‑valuation for watches under $100,000. You assign the insured value based on purchase price or current market research, upload photos, and coverage begins immediately.

Hodinkee also includes appreciation protection, paying up to 150% of the insured value if market prices rise before a loss occurs.

CTA

Compare Hodinkee Insurance against other luxury watch insurers to see how coverage limits, deductibles, and appreciation protection stack up.

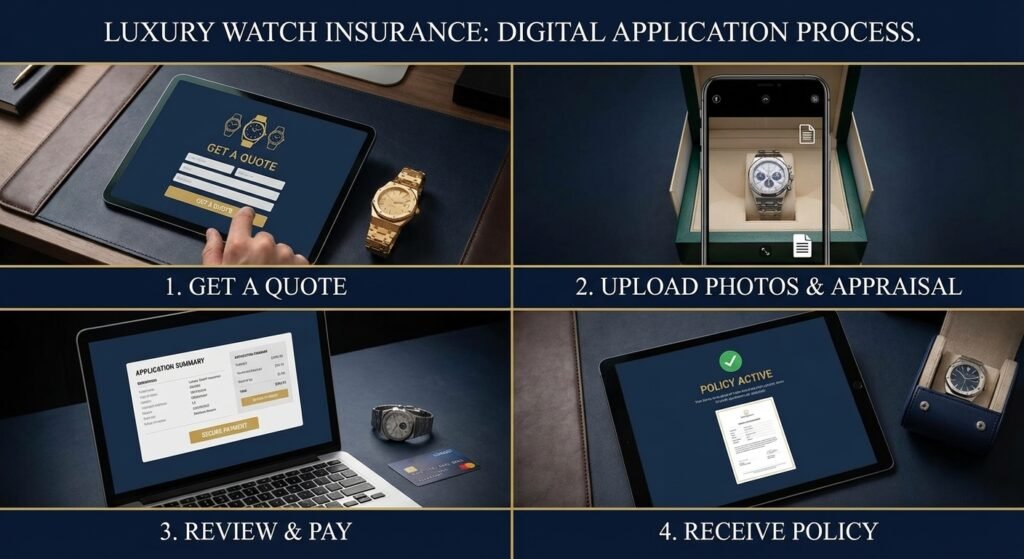

The Application Process: Speed vs. Thoroughness

The application process is fast. Adding watches, uploading photos, and receiving quotes typically takes only a few minutes.

Coverage activates immediately upon payment, which is useful if you’ve just purchased a watch or are about to travel.

For watches over $100,000, formal appraisals are required, but Hodinkee allows a 90‑day grace period after coverage begins.

Accurate self‑valuation is essential. Research current market prices carefully to avoid under‑ or over‑insuring your watches.

Coverage Limits and Exclusions: The Fine Print

Wear and tear, gradual deterioration, and mechanical failure from normal use are excluded.

Damage from insects, vermin, inherent defects, war, terrorism, and government confiscation are also excluded.

Mysterious disappearance coverage varies by state, which is not always clearly disclosed during the quote process.

Losses must be reported promptly. Delays can result in claim denial.

CTA

Get real insurance quotes to see how exclusions and coverage limits differ between Hodinkee and other luxury watch insurers.

Claims Experience: Where Theory Meets Reality

Claims experiences vary. Some collectors report fast settlements within days.

However, Better Business Bureau complaints highlight issues with delayed responses and difficulty reaching customer service.

Some complaints involve billing disputes and unexpected renewals, while others cite long response times for coverage questions.

These inconsistencies suggest growing pains in customer service infrastructure.

Pricing Analysis: Value for Money

Premiums typically range from 0.7% to 1.3% of insured value annually.

A $50,000 collection may cost $350–$650 per year, while a $150,000 collection may cost $1,050–$1,950.

Zero deductibles add value, especially when claims occur, but pricing varies by location and theft risk.

Who Should Consider Hodinkee Insurance

Hodinkee works best for collectors with collections between $20,000 and $200,000 who travel frequently and are comfortable managing coverage digitally.

Collectors with ultra‑high‑value pieces may prefer traditional high‑net‑worth insurers offering white‑glove service.

Hodinkee is only available to U.S. residents.

CTA 3

If you travel often with valuable watches, review Hodinkee Insurance carefully to decide whether its digital‑first coverage fits your collection.

Frequently Asked Questions

Does Hodinkee Insurance cover watches outside the United States?

Yes, coverage applies worldwide, but policyholders must have a U.S. primary residence.

What happens if my watch appreciates after I insure it?

Hodinkee covers appreciation up to 150% of the original insured value.

Can I insure vintage watches?

Yes, using self‑valuation based on current market data.

Does Hodinkee require appraisals?

Only for watches over $100,000, with a 90‑day grace period.

Does Hodinkee cover wear and tear?

No. Coverage applies only to sudden and accidental damage.

Key Takeaways

Hodinkee Insurance offers fast, worldwide, all‑risk coverage with zero deductibles and appreciation protection.

Its strengths lie in digital convenience and flexible valuation, while customer service responsiveness remains a concern for some use

Real Conclusion

Choosing the right luxury watch insurance ultimately comes down to how you use and value your collection.